米国の電気自動車(EV)市場が一時的な停滞期を迎える中、GMはBESS市場への投資を強化し、事業ポートフォリオの多角化を進めています。2026年6月に開催された「GM Empower」イベントにおいて、同社はデータセンターや電力事業者向けの次世代蓄電技術として「ナトリウムイオン電池」を最優先で採用する方針を打ち出しました。

EV向けには高いエネルギー密度を持つリチウムイオン電池(LiB)を維持しつつ、定置型蓄電には「用途に最適な化学組成を選ぶ」という方針のもと、コストとサプライチェーンの安定性に優れたナトリウムイオン電池を選択。2028年初頭の量産出荷を目指し、米国国内での開発・製造エコシステムの構築を急いでいます。

- GMがBESSにナトリウムイオン電池を採用する4つの理由

- 関連情報:ナトリウムイオン電池を巡るグローバル市場と技術の現状

- 主要バッテリー特性の比較

- まとめと今後のタイムライン

- Why GM is Fully Adopting Sodium-ion Batteries for BESS and Its 2028 Mass Production Strategy

- 4 Reasons Why GM is Adopting Sodium-ion Batteries for BESS

- Related Information: Global Market and Technical Status of Sodium-ion Batteries

- Comparison of Major Battery Characteristics

- Summary and Future Timeline

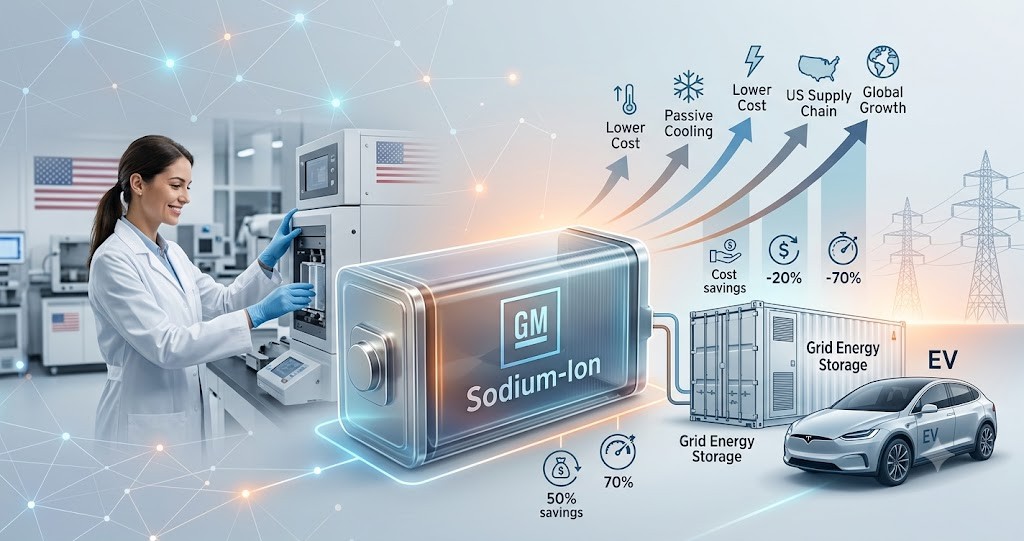

GMがBESSにナトリウムイオン電池を採用する4つの理由

1. 圧倒的な低コスト化とシステムレベルの簡素化

ナトリウムイオン電池は、リチウムイオン電池に比べて作動温度域が広く、熱安定性に優れています。Peak Energyが開発するシステムでは「受動冷却(パッシブ冷却)」を採用しており、従来のLiBで不可欠だった複雑な液体冷却システムや可動部品、定期メンテナンスを排除できます。

これにより、冷却による電力ロスが減るだけでなく、BESSプログラムのライフサイクル全体におけるエネルギー貯蔵コストを最大40%削減することが可能になります。

2. サプライチェーンの強靭化と「脱・中国依存」

リチウムやコバルト、ニッケルといったLiBの主要材料は地理的偏在性が高く、特に製錬・加工インフラは中国が圧倒的なシェアを握っています。一方、ナトリウムは地球上に豊富に存在する塩(NaCl)などから容易に調達できるため、材料コストを抑え、地政学的リスクを回避した強靭なサプライチェーンを構築できます。

3. 米国国内における技術主権の確立

GMは他国の技術をライセンス導入するのではなく、ミシガン州の自社バッテリー研究所でナトリウムイオン電池の設計・開発を行い、製造に関する独占権を保持します。これにより、米国国内で蓄積したリチウムイオン電池の試作・工業化ノウハウをそのまま応用しつつ、独自の知財(IP)に基づいた国内生産基盤を確立します。

4. 技術の「伸び代」と長期的な将来性

成熟期を迎えているNMC(ニッケルマンガンコバルト)やLFP(リン酸鉄リチウム)に対し、ナトリウムイオン電池はまだ商業化の初期段階にあります。それゆえに今後の材料改善やプロセス革新による性能向上の余地(伸び代)が大きく、将来的に既存の電池を凌駕する可能性を秘めています。

関連情報:ナトリウムイオン電池を巡るグローバル市場と技術の現状

GMの参入背景をより深く理解するために、現在のナトリウムイオン電池(SIB)に関する市場環境と技術的課題の関連情報を補足します。

中国勢の先行とグローバル開発競争

SIBの商業化において、現時点では中国企業(CATLやHiNa Batteryなど)が量産化で世界をリードしています。CATLはすでに第一世代のナトリウムイオン電池(エネルギー密度 160Wh/kg)を発表しており、第2世代では 200Wh/kg を目標に掲げています。GMがPeak Energyと組み、ミシガン州で独自開発を進める背景には、この分野での中国独占を阻止し、北米内での経済主権を確保する強い狙いがあります。

負極材(ハードカーボン)と電解液の技術革新

ナトリウムイオンはリチウムイオンに比べてイオン半径が大きいため、LiBの一般的な負極材料である黒鉛(グラファイト)の層間に入り込むことができません。そのため、SIBでは「ハードカーボン(難黒鉛化性炭素)」と呼ばれる特殊な炭素材料が必須となります。現在、このハードカーボンの低コスト製造技術や、低温・高温特性をさらに高めるための特殊な電解液添加剤(LiFSIやLiDFOB、あるいはナトリウム塩を用いたNaFSIなど)の開発が、電池の長寿命化に向けた世界的なトレンドとなっています。

主要バッテリー特性の比較

データセンターや大規模電力貯蔵(BESS)の視点から、ナトリウムイオン電池と、現在定置型で主流のLFP(リン酸鉄リチウム)電池の特性を比較します。

| 評価項目 | ナトリウムイオン電池(SIB) | リン酸鉄リチウム電池(LFP) |

| 資源の豊富さ | 極めて高い(塩などから広く入手可能) | 中程度(リチウムやリンの埋蔵量に依存) |

| 原材料コスト | 低い(高価なレアメタルが不要) | リチウム価格の市場変動に影響されやすい |

| 熱安定性・安全性 | 非常に優れる(熱暴走リスクが低い) | 比較的高いが、厳密な熱管理が必要 |

| 動作温度範囲 | 広い(極低温から高温まで性能を維持) | 狭い(特に低温環境で容量が低下) |

| エネルギー密度 | 比較的低い(140-160Wh/kg 程度) | 中程度(160-200Wh/kg 程度) |

| 冷却・メンテ | 最小限(パッシブ冷却による簡素化が可能) | 中から高(アクティブ液体冷却が必要) |

| 最適な用途 | 設置面積に制約の少ない系統用・定置型蓄電 | 定置型蓄電、電気自動車(EV) |

まとめと今後のタイムライン

GMのナトリウムイオン戦略は、単なるEVの補完計画ではなく、電力会社やデータセンターの爆発的な電力需要(AI需要の拡大など)を見据えた長期的なインフラビジネスへの本格参入を意味しています。

- 2026年現在:定置型蓄電専用セルのプロトタイプ試作および実証試験を実施中。

- 2028年初頭:新設の電池開発センターから、初の量産型ナトリウムイオン電池の出荷を開始予定。

既存のLiB開発で培った米国内の製造・エンジニアリング資産をレバレッジしながら、受動冷却によるシステムコスト40%削減というPeak Energyの強みを融合させることで、GMは次世代クリーンエネルギー市場における主導権獲得を狙っています。

Why GM is Fully Adopting Sodium-ion Batteries for BESS and Its 2028 Mass Production Strategy

As the US electric vehicle (EV) market enters a temporary cooling-off period, GM is strengthening its investment in the BESS market to diversify its business portfolio. At the “GM Empower” event held in June 2026, the company announced a policy to prioritize the adoption of “sodium-ion batteries” as a next-generation energy storage technology for data centers and electric utilities.

While maintaining high-energy-density lithium-ion batteries (LiB) for EVs, GM has chosen sodium-ion batteries—which offer excellent cost efficiency and supply chain resilience—based on its core principle of “selecting the optimal chemistry for the application” in stationary storage. Aiming for mass production shipments by early 2028, the company is accelerating the establishment of a domestic development and manufacturing ecosystem in the United States.

4 Reasons Why GM is Adopting Sodium-ion Batteries for BESS

1. Overwhelming Cost Reduction and System-Level Simplification

Sodium-ion batteries operate across a wider temperature range and exhibit superior thermal stability compared to lithium-ion batteries. The system being developed by Peak Energy utilizes “passive cooling,” which eliminates the complex liquid cooling systems, moving parts, and routine maintenance that are indispensable for conventional LiBs.

This setup not only reduces parasitic power loss from cooling but also enables up to a 40% reduction in energy storage costs over the entire lifecycle of the BESS program.

2. Supply Chain Resilience and “Reducing Dependence on China”

The primary raw materials for LiBs, such as lithium, cobalt, and nickel, are geographically concentrated, and China holds an overwhelming share of the refining and processing infrastructure. In contrast, sodium can be easily sourced from abundant materials like common salt (NaCl). This allows GM to suppress material costs and build a resilient supply chain that avoids geopolitical risks.

3. Establishing Technological Sovereignty in the US

Rather than licensing technology from foreign companies, GM will design and develop sodium-ion batteries at its own battery lab in Michigan, retaining exclusive manufacturing rights. This approach allows GM to directly apply its accumulated US-based expertise in lithium-ion battery prototyping and industrialization while establishing a domestic production foundation grounded in its own intellectual property (IP).

4. Room for Technological Growth and Long-Term Potential

While NMC (nickel manganese cobalt) and LFP (lithium iron phosphate) are considered mature technologies, sodium-ion batteries are still in the early stages of commercialization. Consequently, there is significant headroom for performance improvements through future material optimization and process innovations, giving them the potential to surpass existing batteries in the long run.

Related Information: Global Market and Technical Status of Sodium-ion Batteries

To provide a deeper understanding of GM’s entry into this space, here is supplementary information regarding the current market environment and technical challenges surrounding sodium-ion batteries (SIB).

Leadership of Chinese Players and the Global Development Race

In terms of SIB commercialization, Chinese companies (such as CATL and HiNa Battery) currently lead the world in mass production. CATL has already announced its first-generation sodium-ion battery with an energy density of 160Wh/kg and aims for 200Wh/kg in its second generation. GM’s strategy to partner with Peak Energy and pursue independent development in Michigan is strongly driven by the desire to prevent a Chinese monopoly in this sector and secure economic sovereignty within North America.

Technical Innovations in Anode Materials (Hard Carbon) and Electrolytes

Because sodium ions have a larger ionic radius than lithium ions, they cannot intercalate between the layers of graphite, which is the standard anode material for LiBs. Therefore, SIBs require a specialized carbon material called “hard carbon” (non-graphitizable carbon). Currently, global development trends focus on low-cost manufacturing technologies for hard carbon, as well as specialized electrolyte additives (such as LiFSI, LiDFOB, or sodium-based NaFSI) to enhance high- and low-temperature performance and extend battery cycle life.

Comparison of Major Battery Characteristics

From the perspective of data centers and large-scale utility energy storage (BESS), the table below compares the characteristics of sodium-ion batteries and LFP (lithium iron phosphate) batteries, which are currently the mainstream choice for stationary storage.

| Evaluation Item | Sodium-ion Battery (SIB) | Lithium Iron Phosphate Battery (LFP) |

| Abundance of Resources | Extremely High (widely available from salt, etc.) | Moderate (dependent on lithium and phosphorus reserves) |

| Raw Material Cost | Low (no expensive rare metals required) | Highly susceptible to market fluctuations in lithium prices |

| Thermal Stability & Safety | Excellent (low risk of thermal runaway) | Relatively high, but requires strict thermal management |

| Operating Temperature Range | Wide (maintains performance from extreme cold to heat) | Narrow (capacity drops significantly in cold environments) |

| Energy Density | Relatively Low (around 140-160Wh/kg) | Moderate (around 160-200Wh/kg) |

| Cooling & Maintenance | Minimal (simplification via passive cooling is possible) | Moderate to High (active liquid cooling is required) |

| Optimal Use Case | Utility-scale and stationary storage with fewer footprint constraints | Stationary storage and Electric Vehicles (EVs) |

Summary and Future Timeline

GM’s sodium-ion strategy is not merely a supplementary plan for its EV business; it represents a full-scale entry into the long-term infrastructure market, targeting the explosive power demands of utilities and data centers driven by AI expansion.

- As of 2026: Prototyping and verification testing of cells dedicated to stationary storage are currently underway.

- Early 2028: Shipments of the first mass-produced sodium-ion batteries are scheduled to begin from the newly established battery development center.

By leveraging its existing US manufacturing and engineering assets developed through LiB production and combining them with Peak Energy’s strength in reducing system costs by 40% via passive cooling, GM aims to capture a leading position in the next-generation clean energy market.

コメント