AIデータセンターの爆発的な増加や電力網(グリッド)の近代化に伴い、世界中で蓄電池システム(BESS)の需要が急増しています。しかし、現在の市場を支配するリチウムイオン電池(LiB)は、原材料の精錬や製造サプライチェーンの大部分を中国に依存しており、これが米国の国家安全保障上の大きなリスクとなっています。

この課題を解決するため、2026年6月、米国の主要なクリーンテック企業や材料サプライヤーが結集し、「米国電池リーダーシップ連合(ABLC:American Battery Leadership Coalition)」を発足させました。本連合は、リチウムに依存しない「ナトリウムイオン電池(SIB)」を米国の国家優先事項として位置づけ、連邦政府による政策支援や資金投入を促すための強力な提言活動を開始しました。

- 米国電池リーダーシップ連合(ABLC)発足の背景と目的

- 関連情報:定置型蓄電におけるナトリウムイオン電池の経済的優位性

- 関連情報:激化するナトリウムイオン電池のグローバル開発競争

- 主要な注目ポイントと今後の展開

- Background and Objectives of the ABLC Launch

- Related Information: Economic Advantages of Sodium-ion Batteries in Stationary Storage

- Related Information: Intensifying Global Competition in Sodium-ion Batteries

- Key Priorities and Future Outlook

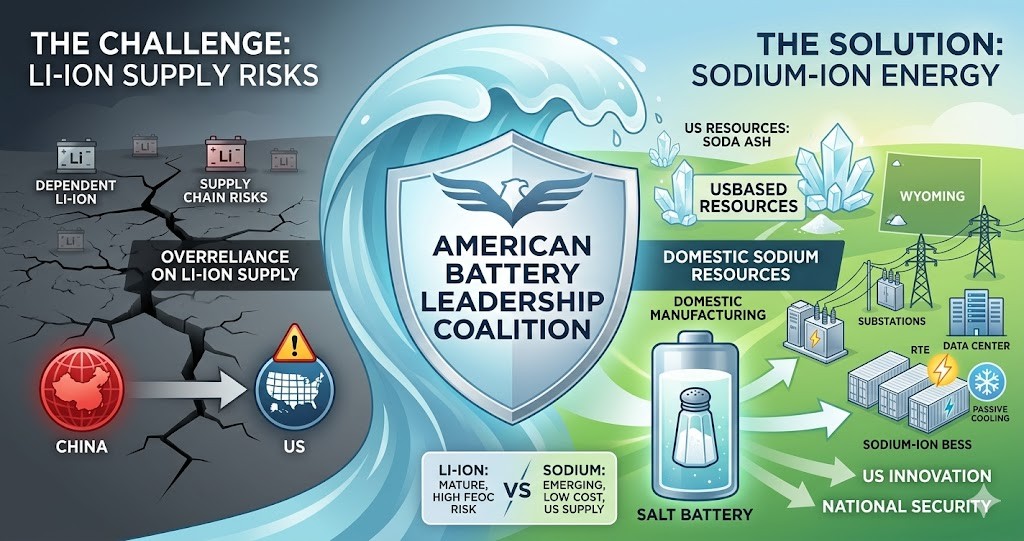

米国電池リーダーシップ連合(ABLC)発足の背景と目的

1. ナトリウムイオン電池を「国家戦略」へ

ABLCは、Alsym EnergyやPeak Energyが主導し、Natron Energy、ESS Tech、Microorousなどのエコシステムを担う主要企業で構成されています。その目的は、ナトリウムイオン技術を米国のエネルギー貯蔵、製造競争力、そして国家安全保障戦略に不可欠なものとして確立することです。

2. 現行政策の「リチウム偏重」という盲点の解消

現在、米国の連邦政府による電池開発助成金の90%以上が、すでに技術的に成熟したリチウム系プロジェクトに投入されています。ABLCは、この政策の盲点を指摘し、法的な認知の拡大、製造奨励策の適用範囲変更、ナトリウムイオン専用の補助金・研究開発パイロット資金の確保を求めています。

3. 国内の非外国企業(FEOC)サプライチェーンの構築

中国をはじめとする「懸念される外国事業体(FEOC)」への依存を排除し、採掘から中間処理、セル製造、システム統合までをすべて北米内で完結させる、完全にクリーンな国内サプライチェーンの確立を目指します。

関連情報:定置型蓄電におけるナトリウムイオン電池の経済的優位性

ABLCがナトリウムイオン電池を「次なるフロンティア」と呼び、政府に強力なプッシュを行う背景には、技術的および構造的な明確な強みがあります。

- 米国が持つ資源の優位性 ナトリウムイオン電池の主要原料であるソーダ灰(炭酸ナトリウム)は、米国(特にワイオミング州など)に世界最大級の埋蔵量があります。レアメタルや中国依存のリチウムとは異なり、国内に確固たる資源基盤があることが、米国にとって最大の構造的競争優位性となります。

- 定置型蓄電(BESS)に特化した優れた経済性 LiBに比べてエネルギー密度はやや低いものの、以下の特徴を持つため、設置面積の制約が少ない系統用蓄電には最も適しています。

- 低運用コストと長寿命:パッシブ冷却(受動冷却)が可能で、システムを簡素化できるため、維持費が大幅に下がります。

- 高い安全性:完全放電(0V状態)での輸送・保管が可能であり、熱暴走のリスクが極めて低いため、データセンターなどの重要インフラに最適です。

- 高い往復効率(RTE):電力の充放電効率が高く、グリッド安定化への貢献度が高い。

関連情報:激化するナトリウムイオン電池のグローバル開発競争

世界市場、特に中国企業との競争環境という視点から、現在の立ち位置を整理します。

中国勢による量産先行

現在、ナトリウムイオン電池の商業生産 capacity は中国(CATLやHiNa Batteryなど)が圧倒的なシェアを握っています。中国勢はすでにEV(小型電気自動車)への搭載や、数十メガワット時規模のBESS実証プロジェクトを次々と立ち上げています。

米国企業による反撃と市場の需要

ナトリウムイオン技術はまだ商業化の初期段階にあるため、標準化や市場の主導権を握るチャンスは米国にも十分残されています。実際、米国企業はすでに総計15ギガワット時(15GWh)を超えるナトリウムイオン蓄電システムの購入計画を発表しており、商業的な需要は十分に存在しています。ABLCは、この限られた「機会の窓」を逃さず、政府の強力なリーダーシップによって国内産業を急成長させる必要があると訴えています。

主要な注目ポイントと今後の展開

ABLCは今後、議会や政策立案者に対して以下の3つの柱を中心に働きかけを行う予定です。

- 中間処理(材料精錬)の規模拡大:国内での原材料加工キャパシティの拡張。

- 需要の喚起と安定化:政府調達ルールを見直し、国内生産されたナトリウムイオン製品を優先的に採用する仕組みの構築。

- 産業政策への統合:AIデータセンターのインフラ整備や、国家の電力網信頼性向上戦略の中に、ナトリウムイオン技術を正式に組み込ませること。

ABLCの発足は、米国がクリーンエネルギー分野における「イノベーション(技術開発)の国」でありながら「製造(量産)の主導権を他国に奪われる」という過去の失敗を繰り返さないための、官民一体となった重要な防衛策といえます。

US Launches “American Battery Leadership Coalition (ABLC)” to Make Sodium-ion a National Strategy

Driven by the explosive growth of AI data centers and the modernization of the electrical grid, global demand for battery energy storage systems (BESS) is surging. However, the lithium-ion battery (LiB) market, which currently dominates the industry, heavily relies on China for raw material refining and the majority of its manufacturing supply chain. This concentration presents a significant national security risk for the United States.

To address this challenge, leading US cleantech companies and material suppliers joined forces in June 2026 to launch the American Battery Leadership Coalition (ABLC). This coalition aims to position lithium-free “sodium-ion batteries” (SIB) as a US national priority and has initiated strong advocacy efforts to secure federal policy support and funding.

Background and Objectives of the ABLC Launch

1. Turning Sodium-ion Technology into a “National Strategy”

Led by Alsym Energy and Peak Energy, the ABLC comprises key ecosystem players, including Natron Energy, ESS Tech, and Microporous. Its primary goal is to establish sodium-ion technology as an indispensable pillar of US energy storage, manufacturing competitiveness, and national security strategy.

2. Resolving the “Lithium Bias” Blind Spot in Current Policies

Currently, more than 90% of federal grants for battery development are directed toward already-mature lithium-based projects. The ABLC highlights this policy blind spot, advocating for expanded legal recognition, broader manufacturing incentives that cover non-lithium chemistries, and dedicated funding pathways for sodium-ion research, pilot projects, and commercialization.

3. Building a Domestic, Non-FEOC Supply Chain

The coalition aims to eliminate reliance on Foreign Entities of Concern (FEOC), such as China, by establishing a completely clean, domestic supply chain within North America that encompasses everything from mining and intermediate processing to cell manufacturing and system integration.

Related Information: Economic Advantages of Sodium-ion Batteries in Stationary Storage

The ABLC’s push to position sodium-ion batteries as the “next frontier” is backed by distinct technical and structural advantages.

- The US Resource Advantage Soda ash (sodium carbonate), the primary raw material for sodium-ion batteries, boasts some of the world’s largest reserves in the United States, particularly in states like Wyoming. Unlike rare earth elements or lithium, which are prone to Chinese supply chain concentration, sodium provides the US with a robust domestic resource base that serves as a major structural competitive edge.

- Superior Economics Tailored for Stationary Storage (BESS) Although sodium-ion batteries have a slightly lower energy density than LiBs, they are exceptionally well-suited for utility-scale storage where physical footprint constraints are less critical, thanks to the following features:

- Low Operating Costs and Long Cycle Life: SIBs allow for passive cooling, which simplifies system architecture and significantly reduces maintenance expenses.

- High Safety Profile: They can be transported and stored at a total state of charge of 0V (fully discharged), and they exhibit a very low risk of thermal runaway, making them ideal for critical infrastructure like data centers.

- High Round-Trip Efficiency (RTE): SIBs deliver strong charge and discharge efficiency, contributing effectively to grid stabilization.

Related Information: Intensifying Global Competition in Sodium-ion Batteries

The current positioning of the US within the global market, especially in comparison to Chinese competitors, highlights the urgency of this initiative.

China’s Head Start in Mass Production

Currently, China holds an overwhelming share of the commercial production capacity for sodium-ion batteries, with giants like CATL and HiNa Battery leading the charge. Chinese players have already begun integrating SIBs into small electric vehicles and deploying multi-megawatt-hour BESS demonstration projects.

US Counteroffensive and Market Demand

Because sodium-ion technology is still in the early stages of commercialization, the window of opportunity remains wide open for the US to capture market leadership and shape global standards. In fact, US companies have already announced procurement plans totaling over 15 gigawatt-hours (15GWh) of sodium-ion storage systems, proving that commercial demand is substantial. The ABLC emphasizes that the US must capitalize on this limited “window of opportunity” through decisive federal leadership to rapidly scale the domestic industry.

Key Priorities and Future Outlook

Moving forward, the ABLC will focus its advocacy efforts toward Congress and policymakers on three main pillars:

- Scaling Up Intermediate Processing: Expanding domestic capacity for raw material refining and chemical processing.

- Stimulating and Stabilizing Demand: Reforming government procurement rules to establish mechanisms that prioritize domestically produced sodium-ion products.

- Integration into Industrial Policy: Ensuring sodium-ion technology is formally incorporated into broader national strategies concerning AI data center infrastructure and grid reliability.

The establishment of the ABLC represents a vital, unified public-private defense mechanism designed to break a historical pattern: ensuring the US does not lose manufacturing and supply chain leadership to foreign rivals in a clean energy sector pioneered by American innovation.

コメント