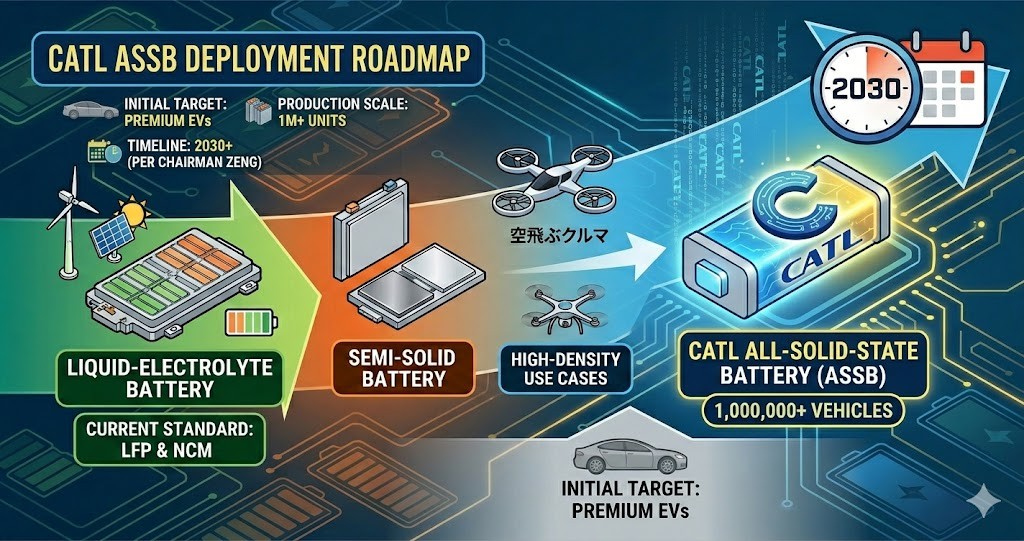

電気自動車(EV)向け駆動用バッテリーで世界首位を走るCATLのロビン・ゼン会長は、次世代技術として期待される「全固体電池」の大規模な商業化(100万台規模の生産)は2030年まで達成できないとの見通しを示しました。

1. 全固体電池の製造ボトルネックと市場投入の現実

全固体電池は、現在主流の液体電解質に比べてエネルギー密度や安全性が飛躍的に向上すると期待されていますが、実用化には高いエンジニアリング上の障壁が存在します。

- 技術成熟度(TRL)の現在地: 9段階評価のうち、現在は「レベル4(実験室での検証・プロトタイプ開発段階)」にすぎません。

- 最大の課題(界面抵抗): 固体同士の接触面(界面)の抵抗を減らすため、6000気圧という超高圧で接合する技術が試みられていますが、材料ごとの密度の違いから構造的なずれが生じ、劣化が早まる問題が解決していません。

- 初期の市場ターゲット: コスト面から、導入初期は車両価格25万元(約36,920米ドル)以上の高級車プラットフォームに限定される見通しです。

- 関連情報(他社の動向): トヨタ自動車や日産自動車なども2020年代後半の全固体電池の実用化を掲げていますが、CATLの見解通り「一般車への普及(大規模量産)」には2030年以降まで時間がかかるとみるのが業界の共通認識となりつつあります。

2. 現在の主流市場:液体電解質(LFPと三元系)の圧倒的優位

全固体電池の量産化に時間がかかるなか、現在のEV市場は実績のある液体電解質バッテリーが支えています。CATLの2026年5月の設備容量は33.08GWhに達し、前月(29.06GWh)から順調に拡大しています。

- 化学組成の2大潮流: 中国市場では、安価で寿命が長い「リン酸鉄リチウム(LFP)電池」がシェアの約7割(5月実績23.12GWh)を占め、エネルギー密度の高い「三元系リチウム電池」(同9.96GWh)を圧倒しています。

- 関連情報(LFPの進化): かつてLFPはエネルギー密度が低いことが弱点でしたが、パック構造の最適化技術(セル・トゥ・パックなど)の向上により、現在では航続距離を十分に確保できるようになり、世界的なデファクトスタンダード(事実上の標準)となっています。

3. 多様化する次世代バッテリーのロードマップ

全固体電池(特にCATLが長期投資する硫化物系)の本格普及を待つ間、自動車・航空宇宙業界では「半固体電池(複合材料構造)」や「代替化学物質」の実用化が先行しています。

- 東風汽車の「酸化物ポリマー電池(半固体)」: 中国の東風汽車は2026年後半に、液体と固体を組み合わせた複合構造のバッテリーを実用化予定です。エネルギー密度350Wh/kg、航続距離1000キロメートル以上を達成し、従来比で重量を30パーセント削減、マイナス30度の極寒環境でも74パーセント以上の容量を維持します。

- 航空宇宙(空飛ぶクルマ)での活用: eVTOL(電動垂直離着陸機)大手のEhangは、深センNeox製の480Wh/kgという超高密度なリチウム金属固体電池を採用し、瓊州海峡の無人飛行に成功しました。

- ナトリウムイオン電池の台頭: リチウムの価格変動リスクやサプライチェーン依存を避けるため、低価格な「ナトリウムイオン電池」などの新プラットフォームの開発も活発化しています。

まとめ:CATLの二段構えの経営戦略

CATLは、将来の本命である硫化物系全固体電池の研究開発に100億元(約14億7600万米ドル)という巨額の長期投資を続ける一方、コスト面で全固体電池が完全に既存品と同等になるまでは、現在の完成された「液体電解質プラットフォーム」を主軸として利益を確保する戦略をとっています。次世代電池への移行は、一歩一歩段階を踏んで進む現実的なシナリオが描かれています。

The Reality of Solid-State Batteries Revealed by CATL Chairman: Mass Production by 2030, and Why They Will Stay “Limited to Luxury Vehicles” for Now

Dr. Robin Zeng, Chairman of CATL—the world’s leading manufacturer of EV driving batteries—has shared a outlook that the large-scale commercialization of next-generation solid-state batteries (defined as production for 1 million vehicles) will not be achieved until 2030.

1. Manufacturing Bottlenecks of Solid-State Batteries and the Reality of Market Launch

While solid-state batteries are expected to drastically improve energy density and safety compared to current mainstream liquid electrolyte batteries, high engineering barriers stand in the way of practical application.

- Current Status of Technology Readiness Level (TRL): On a 9-grade scale, the technology is currently at just “Level 4,” which is limited to laboratory validation and prototype development.

- The Biggest Challenge (Interfacial Resistance): To reduce resistance at the contact surfaces (interfaces) between solids, engineers are testing a method that bonds components under an ultra-high pressure of 6000 atmospheres. However, structural misalignment occurs due to differences in compression density between materials, which accelerates cell degradation. This issue remains unresolved.

- Initial Market Target: Due to high costs, initial deployment will be restricted to luxury vehicle platforms priced at 250000 yuan (approximately 36920 US dollars) or above.

- Related Information (Competitor Trends): Although companies like Toyota and Nissan have announced plans to commercialize solid-state batteries in the late 2020s, a shared understanding is emerging across the industry that widespread adoption for average cars (large-scale mass production) will take until 2030 or later, matching CATL’s view.

2. The Mainstream Market Today: Overwhelming Dominance of Liquid Electrolytes (LFP and Ternary)

As mass production of solid-state batteries takes time, the current EV market continues to rely on proven liquid electrolyte batteries. CATL’s installed capacity reached 33.08 GWh in May 2026, showing steady continuous growth from the 29.06 GWh recorded in April.

- Two Major Trends in Chemical Composition: In the Chinese market, low-cost and long-life Lithium Iron Phosphate (LFP) batteries hold roughly a 70 percent market share (23.12 GWh in May), overwhelmingly outpacing high-energy-density ternary lithium batteries (9.96 GWh in May).

- Related Information (Evolution of LFP): Low energy density used to be the main weakness of LFP batteries. However, thanks to improvements in pack structure optimization technologies (such as cell-to-pack technology), they can now secure ample driving range, becoming a global de facto standard.

3. Diversifying Next-Generation Battery Roadmaps

While waiting for the full-scale commercialization of solid-state batteries (especially the sulfide-based systems that CATL is investing in for the long term), the automotive and aerospace industries are moving ahead with the practical application of “semi-solid-state batteries (composite structures)” and alternative chemical platforms.

- Dongfeng Motor’s Oxide-Polymer Battery (Semi-Solid): China-based Dongfeng Motor plans to deploy a composite structure battery combining liquid and solid elements in late 2026. This pack achieves an energy density of 350 Wh/kg, enables a driving range of over 1000 kilometers on a single charge, reduces total pack weight by 30 percent compared to conventional liquid batteries, and retains over 74 percent of its capacity even in extreme cold conditions of minus 30 degrees Celsius.

- Application in Aerospace (Flying Cars): Ehang, a major player in eVTOL (electric vertical takeoff and landing) aircraft, successfully integrated an ultra-high-density 480 Wh/kg lithium-metal solid-state battery manufactured by Shenzhen Neox to complete an unmanned flight across the Qiongzhou Strait.

- Rise of Sodium-Ion Batteries: To mitigate the risk of lithium price volatility and supply chain dependency, companies are also actively developing new, lower-cost platforms like sodium-ion batteries.

Summary: CATL’s Two-Pronged Corporate Strategy

CATL is continuing its massive, long-term investment of 10 billion yuan (approximately 1.476 billion US dollars) into research and development for sulfide-based solid-state batteries, which it views as the ultimate future solution. At the same time, the company’s strategy focuses on securing profits by using its fully mature liquid electrolyte platform as its main manufacturing foundation until solid-state batteries achieve complete cost parity with existing products. The transition to next-generation batteries is being mapped out as a realistic, step-by-step scenario.

コメント