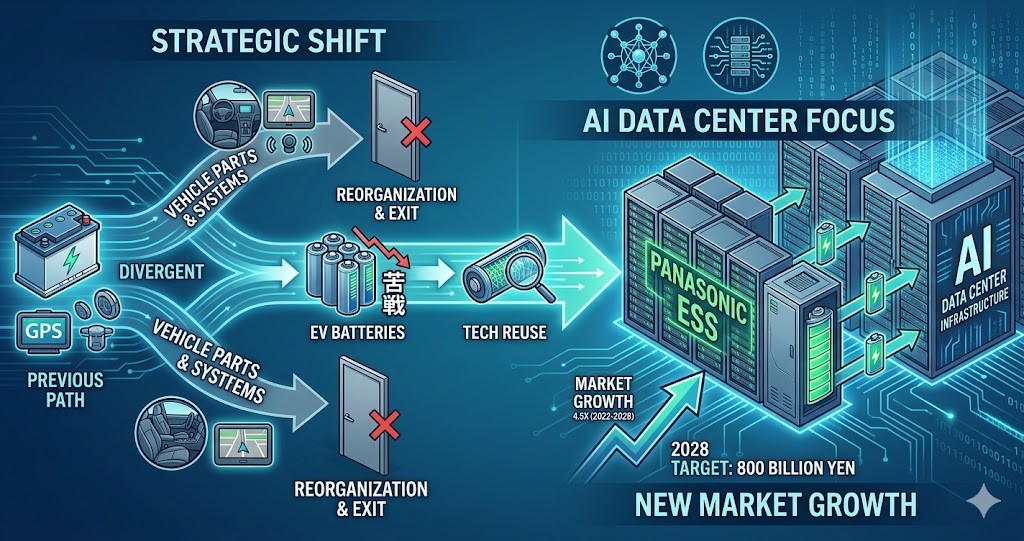

パナソニックホールディングス(HD)は、激変する自動車部品業界において車載機器事業からの撤退・再編を断行する一方、車載電池で培った技術を急成長する「AIデータセンター向け蓄電システム(ESS)」へとシフトさせ、新たな活路を見出しています。

1. 車載機器事業からの撤退と業界再編の背景

パナソニックHDは、カーナビや運転支援システムなどを手がける車載機器事業(パナソニックオートモーティブシステムズ:PAS)の売却を進めてきました。2026年3月にはスペインのフィコサ・インターナショナルの売却も完了し、一連の撤退に区切りをつけています。

- 撤退の要因: 車の電子化(CASE対応)に伴い開発費が巨額化。5000億円以上の売上高がありながら純利益が赤字に沈むなど、競争が激化していました。

- 関連情報(業界の動向): この動きはパナソニックHDに限ったことではありません。三菱電機や日立製作所(旧日立オートモティブシステムズの再編)など、国内の主要電機・機械メーカーも、投資効率の悪い既存の車載部品から、ソフトウェアや次世代領域へリソースをシフトする大規模なポートフォリオ再編を急いでいます。

2. 電池事業の苦戦と「AIインフラ」へのシフト

EV用バッテリーを担うパナソニックエナジーは、かつて米テスラへの独占供給を武器に2019年時点で世界シェアの約30パーセント(3割)を誇っていました。しかし、2026年現在、そのシェアは数パーセントにまで低下しています。

- シェア低下の要因: 中国のCATLやBYDといった海外勢が圧倒的な低価格と量産スピードで市場を席巻し、2社だけで世界シェアの5割強を占めるようになったためです。

- 新たな活路(AIデータセンター需要): 生成AIの爆発的普及に伴い、データセンターの消費電力と「停電対策(バックアップ電源)」が世界的な課題となっています。同社は、車載向けで培った高い安全性と品質を武器に、データセンター向け蓄電システム(ESS)市場への注力を強めています。

3. 蓄電システム(ESS)市場の展望と循環型ビジネス

パナソニックエナジーは、データセンター向け電源システムで既に8割のシェアを確保しており、2028年度には売上高8000億円を目指しています。同社の予測では、ESS市場は2028年までに2022年比で4.5倍に拡大する見通しです。

- 関連情報(ESS市場の競合と課題): データセンター向け蓄電市場は、信頼性が第一に求められるためパナソニックに強みがあります。しかし、この領域にもCATLなどの中国勢が低価格なリン酸鉄リチウム(LFP)電池を引っ提げて猛追を始めており、車載同様の激しい価格競争が予想されます。

- 電池の二次利用(リユース): 市場では、車載用としては寿命を迎えた中古電池を、要求水準が比較的低いESS(蓄電用)として再利用する動き(米GMとレッドウッドマテリアルズの提携など)が加速しています。

- パナソニックの挑戦: 安価な中国勢の新品や、中古リユース品が台頭するなかで、パナソニックが誇る「高寿命・高品質・一元管理体制」という付加価値が、クラウド大手(ハイパースケーラー)にどこまで評価され続けられるかが、今後の成長の鍵となります。

出典:https://merkmal-biz.jp/post/115518

From EV Batteries to AI Batteries! Panasonic’s Major Infrastructure Shift for Survival from a Single-Digit Global Share

Panasonic Holdings (HD) has resolutely executed its withdrawal and restructuring from the automotive equipment business amid a rapidly changing auto parts industry. At the same time, the company is finding a new path forward by shifting its technology cultivated in automotive batteries toward the fast-growing market of Energy Storage Systems (ESS) for AI data centers.

1. Background of the Withdrawal from Automotive Equipment and Industry Restructuring

Panasonic HD has been proceeding with the sale of its automotive equipment business, Panasonic Automotive Systems (PAS), which handles car navigation and driving assistance systems. In March 2026, the company completed the sale of Spain-based Ficosa International, marking a milestone in this series of withdrawals.

- Reasons for Withdrawal: Development costs ballooned due to the shift toward electronic vehicles (CASE readiness). Despite generating sales of over 500 billion yen, intense competition pushed net profits into the red.

- Related Information (Industry Trends): This move is not unique to Panasonic HD. Major domestic electrical and machinery manufacturers, such as Mitsubishi Electric and Hitachi (through the restructuring of the former Hitachi Automotive Systems), are also rushing to execute large-scale portfolio restructurings, shifting resources away from low-investment-efficiency automotive components toward software and next-generation fields.

2. Struggles in the Battery Business and the Shift to “AI Infrastructure”

Panasonic Energy, which is responsible for EV batteries, once boasted a global market share of approximately 30 percent in 2019, driven by its exclusive supply agreement with US-based Tesla. However, as of 2026, its share has dropped to just a few percent.

- Reasons for Share Decline: Overseas competitors, such as China-based CATL and BYD, have dominated the market with overwhelming low prices and mass-production speed. These two companies alone now account for more than 50 percent of the global market share.

- New Path Forward (AI Data Center Demand): With the explosive adoption of generative AI, the power consumption of data centers and power outage countermeasures (backup power supplies) have become global challenges. Weaponizing the high safety and quality it developed for automotive use, Panasonic Energy is intensifying its focus on the ESS market for data centers.

3. Outlook for the Energy Storage System (ESS) Market and Circular Business

Panasonic Energy already secures an 80 percent share in the power supply system market for data centers and aims for sales of 8000 billion yen in fiscal year 2028. The company forecasts that the ESS market will expand to 4.5 times its 2022 size by 2028.

- Related Information (ESS Market Competition and Challenges): Panasonic holds an advantage in the data center storage market because reliability is the top priority. However, Chinese competitors like CATL are already launching fierce pursuits in this space with low-priced Lithium Iron Phosphate (LFP) batteries, signaling an intense price war similar to the automotive sector.

- Secondary Use of Batteries (Reuse): The market is seeing an acceleration in reusing second-hand batteries that have reached the end of their automotive life for ESS (storage use), where performance requirements are relatively lower. The partnership between US-based GM and Redwood Materials symbolizes this trend.

- Panasonic’s Challenge: As cheap new Chinese batteries and second-hand reused products emerge, the key to future growth will be how well hyperscalers (major cloud providers) continue to value Panasonic’s unique selling points: long lifespan, high quality, and integrated management systems.

コメント