電気自動車(EV)の普及に伴い、「ホワイトゴールド(白い金)」とも呼ばれ世界中で争奪戦が繰り広げられているリチウム。過去数年間にわたり激しい価格の乱高下を繰り返してきたリチウム市場ですが、2026年現在、再び大きな局面を迎えています。

本稿では、直近のリチウム価格急騰の背景にある中国の動向や市場の構造を整理するとともに、リチウムという金属の基礎知識や、今後の市場見通しについて分かりやすく解説します。

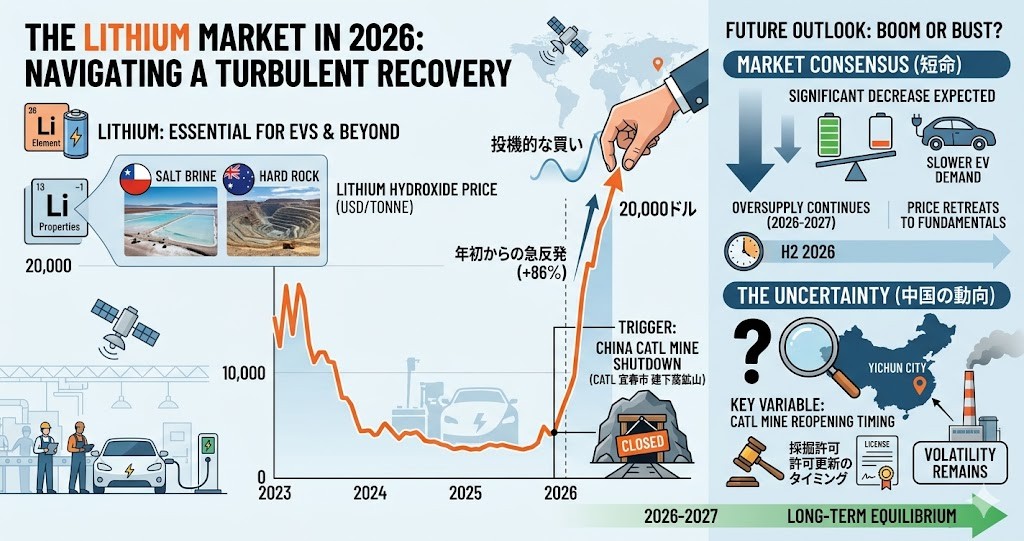

1. そもそもリチウムとは?(関連情報の追加)

リチウム(元素記号:Li、原子番号:3)は、すべての金属の中で最も軽く、かつ最も高い電気化学ポテンシャルを持つアルカリ金属です。この「軽くて電気をたくさん蓄えられる」という性質が、現代のバッテリー技術において不可欠な要素となっています。

主な用途

- リチウムイオン電池: 電気自動車(EV)、スマートフォン、ノートパソコン、定置型蓄電システム(ESS)など。

- 産業用材料: 耐熱ガラス・陶磁器の添加剤、航空宇宙用合金など。

- 潤滑剤: 自動車や産業機械用のグリース(潤滑油)。

供給源の種類

リチウムは主に2つの方法で採掘されます。

- 塩湖水(かん水): 南米のチリやアルゼンチンなどに多く、塩水を蒸発させて回収する。コストは低いが生産に時間がかかる。

- 硬岩鉱床(鉱石): オーストラリアや中国などに多く、スポジュメン(リチウム輝石)やレピドライト(リチウム雲母)などの鉱石から抽出する。建下窩(ジャンシアウォ)鉱山はこのタイプに属します。

2. リチウム市場の現状:突如始まった「再高騰」

長らく底値で低迷していたリチウム価格ですが、2026年に入り急反発を見せています。CME(シカゴ商品取引所)の水酸化リチウム先物価格は年初から86%上昇し、2023年末以来となる1トン当たり2万ドル(20,000ドル)の大台を突破しました。

この急騰の引き金となったのは、世界最大の電池メーカーである中国のCATLが、江西省にある巨大な「建下窩(ジャンシアウォ)鉱山」の操業を停止したことです。採掘許可(ライセンス)の期限切れに伴う一時的な停止とみられていましたが、更新が長引いており、これが市場の供給不安を煽る形となりました。

中国の広州先物取引所では投機的な買いが殺到し、取引量が一時的に膨れ上がりました。現在は取引手数料の引き上げなどで投機熱は落ち着いたものの、価格は依然として高止まりしています。

3. 今後の見通し:再び大暴騰するのか?

市場関係者の多くは、今回の価格高騰は「短命」に終わり、過去のような極端な大ブームにはならないと予測しています。その主な理由は以下の通りです。

供給過剰とEV需要の減速

- EV販売の伸び悩み: 2026年第1四半期の世界の電気自動車(EV)販売台数が期待を下回ったため、通年の需要見通しが下方修正されています。定置型蓄電向けのバッテリー需要は伸びているものの、EVの減速を完全に補うには至っていません。

- 供給の再開: 価格が上昇したことで、これまでの低迷期に稼働を停止していた他の鉱山やプロジェクトが再び動き出します。また、アフリカのジンバブエなどでの供給体制の変化も注視されています。

最大の変動要因は「中国の動向」

BMI(ベンチマーク・ミネラル・インテリジェンス)などの調査機関やBNPパリバ、シティグループなどの金融機関は、現在の価格はファンダメンタルズ(需給の実態)から乖離して割高であると指摘しています。今年後半には「大幅な下落」に転じ、2026年から2027年にかけては供給過剰が続くと予想されています。

今後の焦点は、中国の宜春市当局がいつCATLに新しい採掘許可を出すかです。建下窩鉱山は炭酸リチウム換算で年産15万トンの能力を持つ世界最大級の資産であり、中国の国内供給の安定に不可欠なため、いずれ操業は再開される見込みです。その再開のタイミングが、今後のリチウム価格の動向を左右する最大のカギとなります。

Oversupply Forecasts vs. Recent Surge: The Latest Fundamentals Analysis of the Lithium Market

With the widespread adoption of electric vehicles (EVs), lithium, also known as “white gold,” has sparked a global rush. The lithium market has experienced severe price volatility over the past few years, and as of 2026, it is facing another major turning point. This article outlines the market structure and recent trends in China that triggered the latest price surge. It also provides an easy-to-understand overview of the basics of lithium and its future market outlook.

1. What Is Lithium?

Lithium (element symbol: Li, atomic number: 3) is an alkali metal that is the lightest of all metals and possesses the highest electrochemical potential. This unique characteristic—being lightweight yet capable of storing a massive amount of electricity—makes it an indispensable element in modern battery technology.

Main Applications

- Lithium-ion Batteries: Used in electric vehicles (EVs), smartphones, laptops, and stationary energy storage systems (ESS).

- Industrial Materials: Used as additives for heat-resistant glass and ceramics, as well as in aerospace alloys.

- Lubricants: Used in grease for automobiles and industrial machinery.

Types of Supply Sources

Lithium is primarily extracted through two methods:

- Brine (Salt Lakes): Common in countries like Chile and Argentina in South America. Lithium is recovered by evaporating saltwater. This method has lower costs but takes a long time for production.

- Hard Rock Deposits (Ore): Common in countries like Australia and China. Lithium is extracted from minerals such as spodumene and lepidolite. The Jianxiawo mine belongs to this category.

2. Current State of the Lithium Market: A Sudden “Resurge”

After a prolonged slump at rock-bottom levels, lithium prices have rebounded sharply since the start of 2026. Lithium hydroxide futures on the CME (Chicago Mercantile Exchange) have surged 86% year-to-date, breaking through the major threshold of 20,000 dollars per metric ton for the first time since the end of 2023.

The trigger for this surge was the suspension of operations at the massive Jianxiawo mine in Jiangxi Province by China’s CATL, the world’s largest battery manufacturer. Initially expected to be a temporary shutdown due to the expiration of its mining license, the delay in renewal has fueled supply anxieties in the market.

Speculative buying flooded the Guangzhou Futures Exchange in China, causing trading volumes to temporarily skyrocket. While the speculative frenzy has cooled down following hikes in trading fees and margin requirements, prices still remain high.

3. Future Outlook: Will It Explode Again?

Most market observers predict that this price surge will be short-lived and will not turn into an extreme boom like those seen in the past. The main reasons are as follows:

Oversupply and Slowing EV Demand

- Slowing EV Sales: Global electric vehicle sales in the first quarter of 2026 fell short of expectations, leading to a downward revision of the full-year demand outlook. Although demand for batteries in stationary energy storage is growing, it has not been enough to fully offset the EV slowdown.

- Resumption of Supply: As prices rise, other mines and projects that were halted during the downturn will restart operations. Changes in the supply landscape, such as in Zimbabwe, are also being closely watched.

The Biggest Swing Factor: “China’s Moving Pieces”

Research firms like BMI (Benchmark Mineral Intelligence) and financial institutions including BNP Paribas and Citigroup point out that current prices have disconnected from fundamentals and are overvalued. They forecast a “significant decline” later this year, with oversupply expected to persist through 2026 and 2027.

The immediate focus is on when the local authorities in Yichun, China, will grant a new mining license to CATL. With an annual capacity of 150,000 metric tons of lithium carbonate equivalent, the Jianxiawo mine is one of the world’s largest lithium assets. Since it is vital for China’s domestic supply stability, operations are widely expected to resume eventually. The timing of that restart remains the single biggest catalyst for the future direction of lithium prices.

コメント