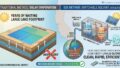

米国のエネルギー貯蔵市場が、かつてない歴史的な急拡大を迎えています。太陽エネルギー産業協会(SEIA)とベンチマーク・ミネラル・インテリジェンスが発表した最新レポート(2026年5月)によると、2026年第1四半期の新規導入容量は前年同期比32%増の9.7 GWh(約10ギガワット時)に達し、第1四半期として過去最高を記録しました。

現在、米国は連邦政府の許認可手続きの遅延(467件の太陽光・蓄電プロジェクトが停滞中)や政治的リスクといった課題に直面しています。しかし、その障壁を遥かに凌駕する「データセンターの爆発的需要」「バッテリーコストの劇的低下」といった強力な市場ドライバーにより、2030年までの累計設置予測は613 GWhへと上方修正されました。本まとめでは、記事が示す5つの主要トレンドに、サプライチェーンや政策動向などの関連情報を補足し、米国の蓄電ビジネスの最前線を俯瞰します。

1. 市場を牽引する5つの主要トレンド

米国の蓄電市場(BESS:バッテリーエネルギー貯蔵システム)の成長は、従来の「再生可能エネルギーの補助」という枠を超え、独立した社会インフラへと脱皮しています。

- データセンターによる「高速電力」需要: 生成AIやハイパースケールコンピューティングの普及により、GoogleやMetaなどのテック大手が数万MWh(メガワット時)規模の蓄電契約を締結しています。送電網の容量不足を回避し、ミリ秒単位の激しい負荷を管理するため、データセンター内に大規模BESSを併設する動きが定着しています。

- トランプ支持州(レッドステート)での経済的自立: 第1四半期に設置された大規模発電容量の71%が、ドナルド・トランプ大統領が勝利した州(ジョージア、アイオワ、ミシシッピなど)に集中しています。党派的なイデオロギーを超え、地域経済の活性化と送電網の信頼性確保という実利が優先されています。

- コストの劇的低下(2022年比55%下落): 製造規模の拡大により、公益事業規模の蓄電平均価格が2022年から55%も急落しました。これによりプロジェクトの採算性が劇的に向上し、蓄電の標準的な持続時間は「平均3時間」で安定しています。

- 「独立型(Stand-alone)蓄電」が過剰半数へ: 従来の「太陽光+蓄電(市場の48%)」のセット導入を抜き、単体で動作する「独立型蓄電」が51%を占めて市場の主役に躍り出ました。電力価格の変動を利用した取引(裁定取引)や系統補助サービスでの収益最大化を狙う開発業者が増えています。

- 国内製造能力の確立: 米国は世界第2位のバッテリー製造国としての地位を固め、23州で工場が稼働・建設中です。現在、セル製造能力で22 GWh(131 GWhが建設中)、パック組立能力で68 GWhを誇っています。

2. 【関連情報】市場をさらに加速・複雑化させる背景

記事のデータを裏付ける、および今後の成長を予測する上で重要な3つの関連情報を補足します。

関連情報①:インフレ抑制法(IRA)の「製造業ボーナス投資税額控除」の恩恵

米国国内での製造能力(セル22 GWh、パック68 GWh)が急速に立ち上がっている背景には、インフレ抑制法(IRA)による強力なインセンティブがあります。米国産材料を一定割合以上使用したプロジェクトには、最大10%の追加税額控除(ドメスティック・コンテンツ・ボーナス)が与えられるため、開発業者はコストが下がった国内産バッテリーの採用を急いでいます。

関連情報②:中国製バッテリーへの関税引き上げとサプライチェーンの現地化

米国政府はエネルギー安全保障の観点から、中国製のEV用および非EV用(定置型含む)リチウムイオンバッテリーに対する関税の大幅な引き上げを進めています。この地政学的リスクを回避するため、テスラや海外大手が米国内での「Megapack」などの生産拠点の新設・増強を急いでおり、これが結果として国内サプライチェーンの数字(建設中の131 GWhなど)を押し上げています。

関連情報③:系統相互接続(インターコネクション)の滞留問題

SEIAの報告書にある「467件のプロジェクトが許認可待ち」という問題の背景には、米国の送電網への接続申請が数年待ちとなる「インターコネクション・キュー(接続待ち行列)」問題があります。この規制上の摩擦があるからこそ、送電網に頼らず自前で電力をコントロールできる「データセンター併設型BESS」や「独立型蓄電」の価値が相対的に高まっています。

結論:2030年に向けた長期展望

米国のエネルギー貯蔵セクターは、規制や政治の壁に揺さぶられながらも、中期的な成長軌道を力強く突き進んでいます。2030年までに、メーター前(電力会社側)の導入量は256%増加し、住宅市場も108%拡大する見通しです。

コストが半分以下に下がったバッテリーは、もはや単なる「再エネのバックアップ」ではなく、国家の「不可欠なエネルギー安全保障インフラ」へと格上げされました。AIデータセンターの爆発的拡大を支え、一般消費者の電気料金高騰を抑えるための防波堤として、BESSを軸とした新しいエネルギー経済圏の構築が米国全土で加速しています。

US Energy Storage Market Achieves Record 10 GWh in a Single Quarter: Energy Security Infrastructure Expanding Rapidly Beyond Political Barriers

The US energy storage market is experiencing an unprecedented and historic expansion. According to the latest report (May 2026) released by the Solar Energy Industries Association (SEIA) and Benchmark Mineral Intelligence, newly installed capacity in the first quarter of 2026 reached 9.7 GWh (approximately 10 gigawatt-hours), a 32% increase compared to the same period last year, marking a record high for any first quarter.

Currently, the United States faces challenges such as delays in federal permitting processes (with 467 solar and storage projects stalled) and political risks. However, driven by powerful market forces that far outweigh these barriers—such as the explosive demand from data centers and a dramatic drop in battery costs—the cumulative installation forecast through 2030 has been revised upward to 613 GWh. This summary provides an overview of the front lines of the US energy storage business, supplementing the five major trends indicated in the article with relevant information on supply chains, policy trends, and other factors.

1. Five Major Trends Driving the Market

The growth of the US energy storage market (BESS: Battery Energy Storage Systems) has evolved beyond the traditional role of “supplementing renewable energy” and is transforming into an independent social infrastructure.

- “Fast Power” Demand Driven by Data Centers: With the spread of generative AI and hyperscale computing, tech giants like Google and Meta are signing massive energy storage contracts on the scale of tens of thousands of MWh (megawatt-hours). To bypass grid capacity shortages and manage intense millisecond-level training loads, the practice of co-locating large-scale BESS within data centers has become firmly established.

- Economic Independence in Trump-Supporting States (Red States): 71% of the large-scale generation capacity installed in the first quarter was concentrated in states won by President Donald Trump (such as Georgia, Iowa, and Mississippi). Transcending partisan ideology, practical benefits such as local economic revitalization and ensuring grid reliability are taking priority.

- Dramatic Cost Reduction (55% Drop Compared to 2022): Due to the expansion of manufacturing scale, the average price of utility-scale energy storage has plummeted by 55% since 2022. This has dramatically improved project profitability, and the standard battery duration for new projects has stabilized at an average of three hours.

- “Stand-alone Storage” Gains the Majority Share: Surpassing the traditional combination of “solar + storage” (which accounts for 48% of the market), “stand-alone storage” operating on its own has taken center stage, capturing 51% of the market. An increasing number of developers are seeking to deploy batteries independently to maximize revenue through energy arbitrage and grid ancillary services.

- Establishment of Domestic Manufacturing Capacity: The United States has solidified its position as the world’s second-largest battery manufacturing country, with factories operating or under construction across 23 states. Currently, the US boasts 22 GWh of operating cell manufacturing capacity (with an additional 131 GWh under construction) and 68 GWh of operating battery pack assembly capacity.

2. [Related Information] Background Accelerating and Complexifying the Market

This section provides three pieces of supplementary information crucial for understanding the data in the article and forecasting future growth.

Related Information 1: Benefits of the Inflation Reduction Act (IRA) “Domestic Content Bonus”

The rapid rise of manufacturing capacity within the United States (22 GWh for cells, 68 GWh for packs) is backed by powerful incentives from the Inflation Reduction Act (IRA). Projects that use a certain percentage of US-made materials receive an additional tax credit of up to 10% (Domestic Content Bonus), prompting developers to quickly adopt domestic batteries with falling costs.

Related Information 2: Increased Tariffs on Chinese Batteries and Localization of the Supply Chain

From an energy security perspective, the US government is moving forward with significant tariff increases on Chinese-made lithium-ion batteries for both EV and non-EV (including stationary) uses. To avoid this geopolitical risk, Tesla and other major overseas companies are rushing to build and expand production bases for products like the “Megapack” within the US. This, in turn, is driving up the figures for the domestic supply chain (such as the 131 GWh currently under construction).

Related Information 3: The Interconnection Queue Bottleneck

The background behind the “467 projects waiting for permits” mentioned in the SEIA report is the “interconnection queue” problem, where applications to connect to the US power grid face multi-year wait times. It is precisely because of this regulatory friction that the value of “data center-located BESS” and “stand-alone storage”—which allow operators to control power locally without relying on the grid—is becoming relatively higher.

Conclusion: Long-Term Outlook Toward 2030

Despite being shaken by regulatory and political hurdles, the US energy storage sector is moving forward strongly on a mid-term growth trajectory. By 2030, front-of-the-meter (utility-side) installations are expected to increase by 256%, and the residential market is predicted to expand by 108% over the same period.

Batteries, with costs reduced by more than half, are no longer just a “backup for renewable energy” but have been elevated to an essential national energy security infrastructure. Serving as a buffer to support the explosive expansion of AI data centers and suppress skyrocketing electricity costs for general consumers, the construction of a new energy economy centered around BESS is accelerating across the United States.

コメント