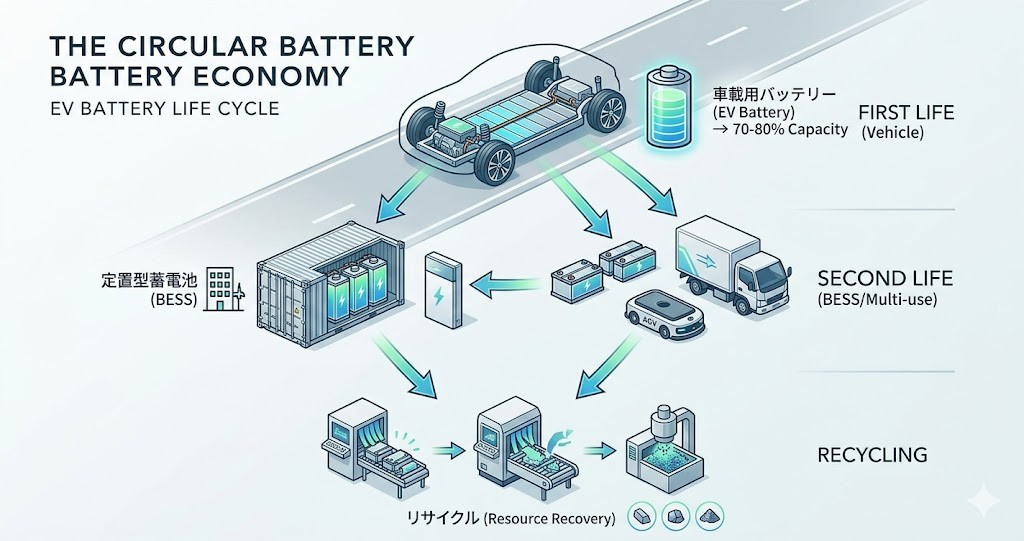

電気自動車(EV)の普及に伴い、その心臓部である「車載用バッテリー」のライフサイクル管理が、自動車産業およびエネルギー産業の最重要テーマとなっています。かつては使用後に即座に分解・リサイクル(資源回収)することが主流と捉えられていましたが、現在ではバッテリーを社会インフラとして長期間活用する「セカンドライフ(リユース)」市場が急速に立ち上がっています。特に米国のインフレ抑制法(IRA)による最大7500ドルの税額控除の終了(2025年9月)に端を発するEV需要の鈍化と、それに伴う電池の余剰生産能力(国内需要182 GWhに対し生産能力275 GWh)は、各社を電力貯蔵システム(BESS)ビジネスへと強く押し出す契機となりました。

本まとめでは、記事で示された各国の動きに、サプライチェーンや技術的背景などの関連情報を補足し、再編が加速するEV電池市場の全体像を俯瞰します。

- 1. 米国発の資源循環とテスラの先行優位

- 2. 日欧が展開する独自のリユース・地域防衛戦略

- 3. 資産価値の最大化(全体管理:バリューチェーンの統合)

- 結論:循環型モビリティ経済の未来

- 1. US-Led Resource Circulation and Tesla’s First-Mover Advantage

- 2. Unique Reuse and Regional Defense Strategies Deployed by Japan and Europe

- 3. Maximizing Asset Value (Total Management: Integration of the Value Chain)

- Conclusion: The Future of a Circular Mobility Economy

1. 米国発の資源循環とテスラの先行優位

米国では、スタートアップや自動車大手が連携し、製造・回収・リユース・リサイクルを繋ぐ巨大なネットワークの構築が進んでいます。

- レッドウッド・マテリアルズの動向: リヴィアンとの提携(2026年4月)により、100個以上の使用済み電池を統合した10 MWh規模の蓄電システムをイリノイ州の工場へ導入。さらにGM(2025年7月提携)、トヨタ、フォード、テスラとも契約を結び、メーカーの枠を超えた資源循環のハブ(交差点)を形成しています。

- テスラの再定義と先行アドバンテージ: テスラは十数年前から家庭用蓄電池「Powerwall」や産業用・系統用蓄電池「Megapack」を展開しており、EVメーカーであると同時にエネルギー企業としての基盤を確立しています。自動車の余剰能力やリユース電池をスムーズにBESSへとシフトできる垂直統合型の強みを持っています。

- 【関連情報】AIデータセンターの爆発的需要: 現在、米国を中心に生成AI用データセンターの建設が急増しており、膨大な電力消費と24時間安定した電源確保が課題となっています。EV電池の技術を応用した大容量BESSは、再生可能エネルギーの出力変動を吸収し、データセンターのバックアップ電源として機能するため、EV市場の減速を補う巨大な受け皿となっています。

2. 日欧が展開する独自のリユース・地域防衛戦略

日本と欧州では、それぞれの地域特性や法規制に合わせたバッテリーの有効活用が進められています。

日本:商用車・多用途への展開と品質基準づくり

- 三菱ふそう & CONNEXX SYSTEMS: 電気小型トラック「eキャンター」の使用済み電池を蓄電システムへ回す実証実験を開始(2026年実用化目標)。商用車は走行距離が長く管理がしやすいため、セカンドライフへの移行がスムーズです。

- 日産自動車: 2014年という極めて早い段階から「リーフ」の電池再利用事業を推進。蓄電用のみならず、ゴルフカート、工場の無人搬送車(AGV)など多岐にわたる用途を開拓。

- 【関連情報】日本の課題と強み: 日本は材料の評価技術や品質管理に優れており、中古バッテリーの「残価測定(SOH:State of Healthの診断)」の標準化で世界をリードしようとしています。これにより、中古電池の資産価値を正しく評価する市場の形成が期待されます。

欧州:再生可能エネルギーの需給調整と強力な法規制

- メルセデス・ベンツ & ルノー・ステランティス: メルセデスは2000個以上の電池を蓄電用に転用。ルノー傘下のMobilizeやステランティスはイタリアで78個の電池を束ねた大規模蓄電拠点を構築。

- 【関連情報】欧州バッテリー規則(EU Battery Regulation)の背景: 欧州でこうした動きが活発な背景には、2020年代半ばから順次導入されている「欧州バッテリー規則」があります。これにはバッテリーの製造から廃棄までの二酸化炭素(CO2)排出量を記録する「バッテリーパスポート」の義務化や、リサイクル素材の最低使用比率の規定が含まれており、自動車メーカーは最初からセカンドライフやリサイクルを組み込んだ設計を強制されています。

3. 資産価値の最大化(全体管理:バリューチェーンの統合)

EV電池ビジネスは、もはや「車を売って終わり」のビジネスモデルを完全に過去のものにしようとしています。

- LTV(顧客生涯価値)の向上: 航続距離の低下(容量70%から80%への劣化)によって車載用としての役目を終えても、BESS(定置型蓄電池)としては元の容量の半分から3分の2程度あれば十分に機能します。これにより、バッテリーは長期間にわたり利益を生み続ける「貴重な資産」となります。

- 新車価格への好循環: 使い終わった後の「残価(下取り価値)」がBESS市場の拡大によって安定すれば、EVの新車購入時のローンやリース価格を引き下げる効果が生まれます。初期費用の高さがネックとされるEVの普及を、裏側から支える仕組みとなります。

- 【関連情報】技術的課題(パックからセルへの分解コスト): リユースをさらに効率化する上での現在の技術的課題は、メーカーごとに電池パックの形状やセルの化学組成(LFP:リン酸鉄リチウム、三元系など)が異なる点です。これらを束ねて安全に制御するシステム(BMS:バッテリーマネジメントシステム)の高度化や、解体を容易にする設計(デザイン・フォー・リサイクル)の共通化が、今後のコスト競争の鍵を握ります。

結論:循環型モビリティ経済の未来

EV電池のセカンドライフを巡る動きは、単なる環境配慮(持続可能性)の枠を大きく超え、「自動車産業とエネルギー産業の融合」を決定づける主戦場となっています。

材料の調達(アップストリーム)から、車両としての運用(ミドルストリーム)、そしてBESSへのリユースや資源回収(ダウンストリーム)に至るまで、すべてのプロセスを網羅する全体管理(バリューチェーンの最適化)を制した企業が、次世代のモビリティ経済をリードすることになります。使い捨てを前提とせず、価値を何度も循環させ、限界まで使い尽くす――このパラダイムシフトこそが、今後の産業競争の核心です。

出典:https://topics.smt.docomo.ne.jp/article/merkmalbiz/business/merkmalbiz-115103

The End of the Car is the Beginning of Infrastructure: The Next Business Created by EV Battery Reuse

With the spread of electric vehicles (EVs), lifecycle management of the “automotive battery,” which is the heart of the vehicle, has become the most critical theme for both the automotive and energy industries. Previously, the mainstream approach was to immediately dismantle and recycle (recover resources) batteries after use. Today, however, a “second life (reuse)” market that utilizes batteries as social infrastructure over the long term is rapidly emerging. In particular, the slowdown in EV demand triggered by the end of the maximum 7500 dollar tax credit under the US Inflation Reduction Act (IRA) in September 2025, combined with the resulting surplus battery production capacity (275 GWh of production capacity against a domestic demand of 182 GWh), has served as a catalyst pushing companies strongly into the Battery Energy Storage System (BESS) business.

This summary provides an overview of the accelerating reorganization of the EV battery market by supplementing the global movements shown in the article with relevant information such as supply chains and technical backgrounds.

1. US-Led Resource Circulation and Tesla’s First-Mover Advantage

In the United States, startups and major automakers are collaborating to build a massive network connecting manufacturing, collection, reuse, and recycling.

- Redwood Materials’ Movements: Through its partnership with Rivian (April 2026), the company introduced a 10 MWh energy storage system integrating more than 100 used batteries into a factory in Illinois. Furthermore, it has signed contracts with GM (July 2025 partnership), Toyota, Ford, and Tesla, forming a hub (intersection) for resource circulation that transcends manufacturer boundaries.

- Tesla’s Redefinition and First-Mover Advantage: Tesla has been deploying the “Powerwall” for home energy storage and the “Megapack” for industrial and grid-scale storage for over a decade, establishing its foundation as an energy company as well as an EV manufacturer. It possesses a vertically integrated strength that allows it to smoothly shift surplus automotive capacity and reused batteries into the BESS sector.

- [Related Information] Explosive Demand from AI Data Centers: Currently, the construction of generative AI data centers is surging, primarily in the United States, making enormous power consumption and securing a stable 24-hour power supply critical challenges. Large-capacity BESS applying EV battery technology absorbs the output fluctuations of renewable energy and functions as a backup power source for data centers, serving as a massive absorber that compensates for the slowdown in the EV market.

2. Unique Reuse and Regional Defense Strategies Deployed by Japan and Europe

In Japan and Europe, effective battery utilization is being advanced in accordance with respective regional characteristics and legal regulations.

Japan: Expansion into Commercial Vehicles and Multiple Applications, and Creation of Quality Standards

- Mitsubishi Fuso & CONNEXX SYSTEMS: Started a demonstration experiment to divert used batteries from the “eCanter” electric light-duty truck into energy storage systems (aiming for practical application in 2026). Because commercial vehicles have high mileage and are easy to manage, the transition to a second life is smooth.

- Nissan Motor: Promoting the battery reuse business for the “Leaf” from an extremely early stage in 2014. The company has opened up a wide variety of applications, not only for energy storage but also for golf carts and automated guided vehicles (AGVs) in factories.

- [Related Information] Japan’s Challenges and Strengths: Japan excels in material evaluation technology and quality control, and is aiming to lead the world in standardizing “residual value measurement” (SOH: State of Health diagnosis) for used batteries. This is expected to create a market that correctly evaluates the asset value of used batteries.

Europe: Renewable Energy Supply-Demand Adjustments and Strong Legal Regulations

- Mercedes-Benz & Renault / Stellantis: Mercedes has repurposed more than 2000 batteries for energy storage. Mobilize (under Renault) and Stellantis have built a large-scale energy storage hub in Italy by bundling 78 batteries.

- [Related Information] Background of the EU Battery Regulation: The driving force behind these active movements in Europe is the “EU Battery Regulation,” which is being introduced sequentially from the mid-2020s. This includes the mandatory “Battery Passport” to record carbon dioxide (CO2) emissions from manufacturing to disposal, as well as regulations on the minimum usage ratio of recycled materials. Automakers are being forced to design vehicles with second life and recycling integrated from the very beginning.

3. Maximizing Asset Value (Total Management: Integration of the Value Chain)

The EV battery business is completely making the “sell a car and finish” business model a thing of the past.

- Improving LTV (Long-Term Value / Lifetime Value): Even if a battery ends its role for automotive use due to a decrease in driving range (degradation to 70% to 80% capacity), it can function sufficiently for BESS (stationary energy storage) if it retains half to two-thirds of its original capacity. As a result, the battery becomes a “valuable asset” that continues to generate profits over a long period.

- Virtuous Cycle for New Car Prices: If the “residual value” (trade-in value) after use stabilizes through the expansion of the BESS market, it will have the effect of lowering loan or lease prices when purchasing a new EV. This serves as a mechanism that supports the spread of EVs from behind the scenes, addressing the hurdle of high initial costs.

- [Related Information] Technical Challenges (Dismantling Costs from Pack to Cell): The current technical challenge in making reuse more efficient is that battery pack shapes and cell chemical compositions (such as LFP: lithium iron phosphate, or ternary systems) differ by manufacturer. Advanced Battery Management Systems (BMS) to safely bundle and control these, as well as the standardization of designs that facilitate dismantling (Design for Recycling), will hold the key to future cost competitiveness.

Conclusion: The Future of a Circular Mobility Economy

Movements surrounding the second life of EV batteries go far beyond the scope of simple environmental consideration (sustainability) and have become the ultimate battleground determining the “fusion of the automotive and energy industries.”

From material procurement (upstream) to vehicle operation (midstream), and finally to BESS reuse and resource recovery (downstream), companies that master total management (optimization of the value chain) covering all processes will lead the next-generation mobility economy. Not assuming disposability, but circulating value over and over again to use it to its absolute limits—this paradigm shift is the core of future industrial competition.

コメント