パナソニックホールディングス(HD)が発表した2025年度第3四半期決算は、EV市場の過渡期における「攻め」と「守り」の転換点を象徴するものとなりました。北米でのEV補助金終了や戦略パートナーのモデル再編といった逆風に対し、同社はデータセンター向け蓄電池という新たな成長エンジンでこれを補完。さらに、1万2,000人規模に及ぶ大規模な構造改革を断行し、次なる成長フェーズへの地ならしを急いでいます。

本決算の内容を整理し、関連情報を交えて詳しく解説します。

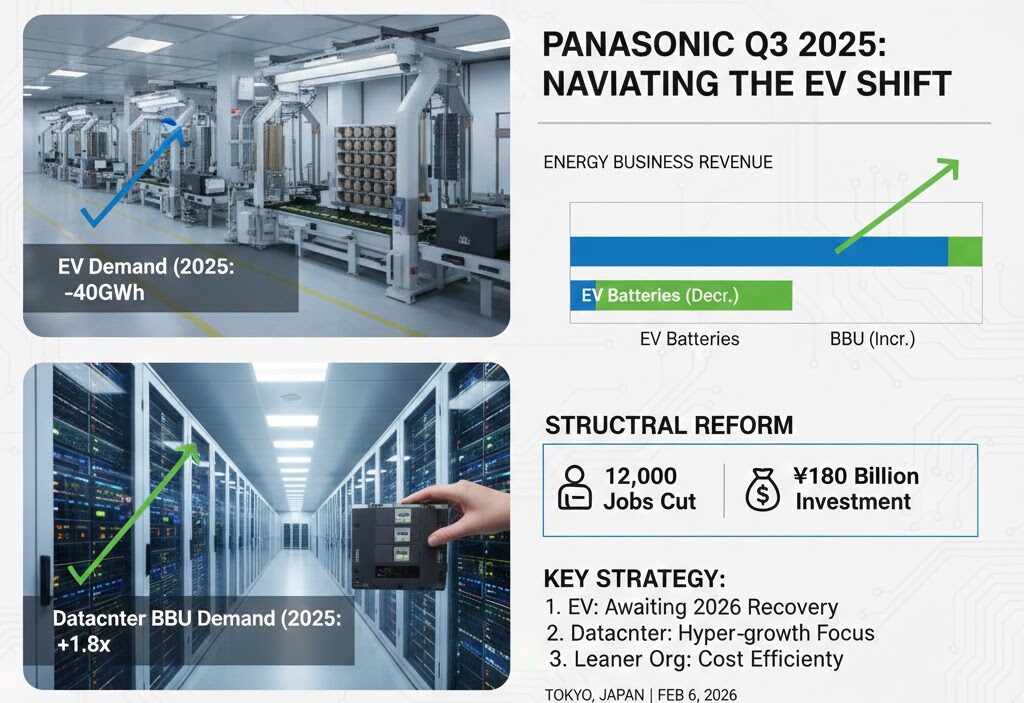

- 1. エナジー事業:EVの「踊り場」をデータセンターが救う

- 2. 構造改革:1.2万人削減と1,800億円の投下

- 3. 2025年度 第3四半期(10-12月)実績と通期見通し

- まとめ:パナソニックが描く「ポストEV偏重」の戦略

- Panasonic Repurposes Domestic EV Battery Lines for Data Center BBU: “Agile Management” in Response to Market Shifts

1. エナジー事業:EVの「踊り場」をデータセンターが救う

車載電池の需要が一時的に減速する一方で、AI需要の爆発に支えられた「産業・民生」部門が好調です。

車載電池:2025年度Q3が「底」との見方

- 現状: 米国のEV補助金(IRA 30D)終了に伴う駆け込み需要の反動、および北米工場の減販により、通期の販売見通しを40GWhから39GWhへ下方修正。

- テスラの動向: 「モデルS/X」の生産終了は「織り込み済み」とし、今後は国内拠点でマツダやスバル向けの供給を模索します。

- 回復のシナリオ: 和仁古CFOは「2026年度に向けて緩やかに回復し、前年並みまで戻る」と予測。ルシッドやズークスなど、新規顧客への供給開始も進めます。

データセンター向けBBU(蓄電ユニット):驚異的な成長

- 上方修正: 年間の売上見通しを期初の「1.5倍」から「1.8倍」へと再修正。

- 野心的な目標: 2028年度までに売上を5,000億円上積みし、8,000億円規模(現在の約3倍近く)を目指します。

- アセット転換: 国内の車載電池ラインをBBU向けに転用するほか、メキシコでの新工場建設も決定。EVの空き枠をデータセンター向けに振り向ける「スピード経営」で稼働率を維持します。

2. 構造改革:1.2万人削減と1,800億円の投下

パナソニックHDは、収益体質の抜本的改善に向け、当初の想定を上回る規模で人員削減とコストカットを断行します。

| 項目 | 当初計画 | 修正後(今回) | 備考 |

| 人員削減規模 | 約10,000人 | 12,000人 | インダストリー・HD部門が中心 |

| 構造改革費用 | 1,500億円 | 1,800億円 | 300億円の積み増し |

| 累計削減効果 | 1,320億円 | 1,450億円 | 2026年度までの2年間累計 |

【補足】 車載電池を扱う「エナジー」部門は成長分野と位置づけられており、今回の人員削減(構造改革費用)の対象からは外れています。

3. 2025年度 第3四半期(10-12月)実績と通期見通し

エナジー事業の数値は、売上増・利益減という、投資フェーズ特有の様相を呈しています。

エナジー事業の実績(Q3単体)

- 売上高: 2,628億円(前年同期比 +22%)

- 調整後営業利益: 417億円(同 9億円減)

- 背景: 北米EV工場の減販影響を、産業向けBBUの利益でカバーしきれなかった形。

2025年度 通期見通し(修正)

- 売上高: 9,520億円(前回比+190億円、前年比 +9%)

- 調整後営業利益: 1,140億円(前回据え置き、前年比 87億円減)

まとめ:パナソニックが描く「ポストEV偏重」の戦略

今回の決算からは、テスラ一本足打法からの脱却と、AIインフラ市場への迅速なシフトが見て取れます。

- EV市場: 2025年末を底に、2026年度の緩やかな回復を待つ。

- データセンター: 最優先投資領域として、生産拠点をメキシコ等へ拡大。

- 筋肉質な組織へ: 1.2万人の人員削減により、固定費を削り利益率を向上させる。

車載電池の苦戦をデータセンターで補う「ポートフォリオの柔軟性」が、今後のV字回復の鍵を握りそうです。

出典:https://car.watch.impress.co.jp/docs/news/2083594.html

Panasonic Repurposes Domestic EV Battery Lines for Data Center BBU: “Agile Management” in Response to Market Shifts

The FY2025 Q3 financial results announced by Panasonic Holdings (HD) mark a symbolic turning point between “offense” and “defense” in a transitional EV market. Facing headwinds such as the end of U.S. EV subsidies and model restructuring by strategic partners, the company is pivoting to data center storage batteries as a new growth engine. Simultaneously, it is pushing through a large-scale restructuring involving 12,000 job cuts to pave the way for its next growth phase.

The following is a detailed breakdown of the financial results and related strategic insights.

1. Energy Business: Data Centers Rescue the EV “Stall”

While demand for EV batteries has temporarily slowed, the “Industrial and Consumer” segment is thriving, fueled by the explosion in AI-related demand.

EV Batteries: Q3 FY2025 Seen as the “Bottom”

- Current Status: Due to a reaction following the rush demand before the end of the U.S. EV tax credit (IRA 30D) and reduced sales at North American plants, the full-year sales forecast has been revised down from 40GWh to 39GWh.

- Tesla’s Strategy: The discontinuation of “Model S/X” production is considered “already priced in.” Moving forward, Panasonic will seek to supply Mazda and Subaru using its domestic Japanese bases.

- Recovery Scenario: CFO Akihito Waniko predicts a “gradual recovery toward FY2026, returning to previous year levels.” The company is also initiating supply to new North American clients such as Lucid and Zoox.

Data Center BBUs (Battery Backup Units): Explosive Growth

- Upward Revision: The annual sales forecast has been revised from the initial “1.5x” to “1.8x” year-on-year.

- Ambitious Targets: The company aims to add 500 billion yen to sales by FY2028, reaching a scale of 800 billion yen (nearly triple the current level).

- Asset Repurposing: In addition to converting domestic EV battery lines for BBU production, a new factory in Mexico has been greenlit. This “Agile Management” reallocates idle EV capacity to data centers to maintain high plant utilization.

2. Structural Reform: Cutting 12,000 Jobs and Investing 180 Billion Yen

Panasonic HD is executing deeper-than-expected job cuts and cost reductions to fundamentally improve its profit structure.

| Item | Original Plan | Revised (Current) | Remarks |

| Job Reductions | Approx. 10,000 | 12,000 | Mainly in Industry and HD sectors |

| Restructuring Costs | 150B JPY | 180B JPY | Increase of 30B JPY |

| Cumulative Savings | 132B JPY | 145B JPY | Total for 2 years through FY2026 |

Note: The “Energy” segment (EV batteries) remains designated as a growth area and is excluded from these specific job cuts and restructuring costs.

3. FY2025 Q3 Results and Full-Year Forecast

The Energy business shows a pattern typical of an investment phase: increased revenue but decreased profit.

Energy Business Results (Q3 Standalone)

- Sales: 262.8 billion JPY (+22% YoY)

- Adjusted Operating Profit: 41.7 billion JPY (-0.9 billion JPY YoY)

- Context: Profits from industrial BBUs could not fully offset the impact of reduced sales at North American EV plants.

FY2025 Full-Year Forecast (Revised)

- Sales: 952.0 billion JPY (+19.0B JPY from previous, +9% YoY)

- Adjusted Operating Profit: 114.0 billion JPY (Unchanged, -8.7B JPY YoY)

Conclusion: Panasonic’s “Post-EV Centralized” Strategy

These results reveal a clear shift: moving away from a heavy reliance on Tesla toward the rapidly growing AI infrastructure market.

- EV Market: Anticipating a gradual recovery in FY2026 after hitting bottom at the end of 2025.

- Data Centers: Expanding production bases to Mexico and elsewhere as a top-priority investment area.

- Leaner Organization: Utilizing 12,000 job cuts to slash fixed costs and improve profit margins.

The “portfolio flexibility” to bridge the EV slump with data center demand will be the decisive factor in Panasonic’s upcoming recovery.

コメント