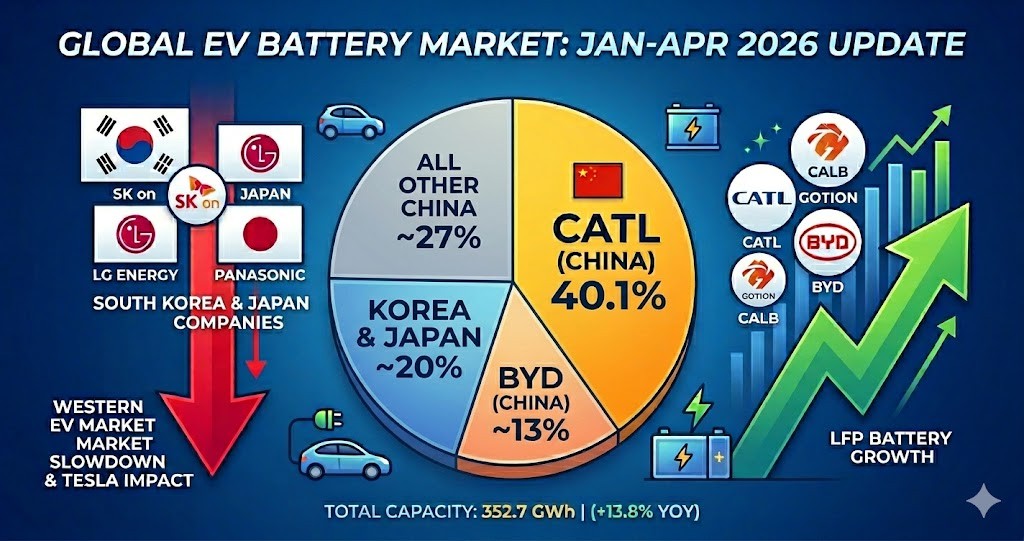

2026年1月から4月までの世界EVバッテリー市場の最新データが公開され、中国メーカーの圧倒的な独占状態がさらに強まっていることが浮き彫りになりました。世界全体のバッテリー使用量が前年同期比13.8パーセント増と堅調に拡大する中、首位のCATLは4割を超えるシェアを確保し、2位のBYDと合わせて市場の過半数を支配しています。かつて市場をリードしていた日本や韓国のメーカーは、主要顧客である欧米EV市場の減速の煽りを受け、苦しい戦いを強いられています。

- 2026年1月~4月 世界EVバッテリー市場シェア(トップ10)

- 発表データから見る重要トピックス

- 【関連情報】理解を深めるための補足

- Global EV Battery Share Jan-Apr 2026: Chinese Players Dominating the Market with 72.2 Percent Share

- Global EV Battery Market Share January-April 2026 (Top 10)

- Key Topics from the Released Data

- Supplementary Context: For Deeper Understanding

2026年1月~4月 世界EVバッテリー市場シェア(トップ10)

市場調査会社SNEリサーチのデータによる、世界の主要EVバッテリーメーカーの業績は以下の通りです。総使用量は352.7GWh(前年同期比13.8パーセント増)に達しました。

| 順位 | 企業名(国籍) | 市場シェア | 設備容量(GWh) | 前年同期比の動向 |

| 1位 | CATL(中国) | 40.1パーセント | 141.4 | 19.8パーセント増(シェア拡大) |

| 2位 | BYD(中国) | 14.2パーセント | 50.0 | 2.4パーセント減(シェア微減) |

| 3位 | LGエナジーソリューション(韓国) | 9.1パーセント | 32.0 | 8.3パーセント増(シェア微減) |

| 4位 | CALB(中国) | 5.1パーセント | 18.1 | 39.3パーセント増(急成長) |

| 5位 | ゴティオンハイテック(中国) | 4.4パーセント | 15.6 | 30.2パーセント増(急成長) |

| 6位 | SKオン(韓国) | 3.5パーセント | 12.3 | 7.9パーセント減(シェア低下) |

| 7位 | パナソニック(日本) | 3.4パーセント | 12.0 | 3.7パーセント減(シェア低下) |

| 8位 | イブ・エナジー(中国) | 3.3パーセント | 11.5 | 30.3パーセント増 |

| 9位 | スボルト(中国) | 2.6パーセント | 9.3 | 37.2パーセント増 |

| 10位 | サンウォダ(中国) | 2.5パーセント | 8.7 | 17.6パーセント増 |

| – | その他 | 11.8パーセント | 41.7 | – |

発表データから見る重要トピックス

1. 中国勢の圧倒的な支配力(トップ10に7社)

トップ10のうち7社を中国企業が占め、その合計シェアは72.2パーセントに達しました(前年同期から2.1パーセントポイント増加)。なかでもCATL(40.1パーセント)とBYD(14.2パーセント)の2強だけで、世界市場の54.3パーセントを占めています。

2. 日韓の主要メーカーの停滞・減少

韓国のSKオン(7.9パーセント減)や、日本のパナソニック(3.7パーセント減)は設置容量そのものが前年を割り込みました。韓国首位のLGエナジーソリューションは設置容量こそ増えたものの、市場全体の成長スピードに追いつけず、シェアを落としています。

【関連情報】理解を深めるための補足

なぜこれほどまでに中国企業が強く、日韓企業が苦戦しているのか、背景にある関連情報を解説します。

日韓企業が苦戦する背景:「欧米EV市場の減速」と「テスラの影響」

- SKオン(韓国)の背景: 主な顧客基盤である北米やヨーロッパにおいて、電気自動車(EV)の販売成長が一時的に鈍化(EVキャズム現象など)している直撃を受けました。

- パナソニック(日本)の背景: 同社の筆頭顧客であるテスラ(Tesla)の特定地域における売上伸び悩みが、そのままバッテリー設置容量の減少に直結しています。パナソニックはテスラへの依存度が極めて高いため、顧客の販売動向が業績を大きく左右する構造になっています。

中国企業が急成長を続ける理由:「LFP電池」の強み

- 中国メーカー(CATL、BYD、CALBなど)は、コバルトやニッケルを使わない安価なLFP(リン酸鉄リチウム)電池の製造に強みを持っています。

- 現在、世界のEV市場では「低価格化」が激しい競争を勝ち抜く最重要テーマとなっており、安くて安全性の高いLFP電池を大量供給できる中国企業に、世界中の自動車メーカーからの注文が集中していることが、シェアのさらなる拡大につながっています。

出典:https://cnevpost.com/2026/06/02/global-ev-battery-market-share-jan-apr-2026/

Global EV Battery Share Jan-Apr 2026: Chinese Players Dominating the Market with 72.2 Percent Share

The latest data for the global electric vehicle (EV) battery market from January to April 2026 has been released, highlighting that the overwhelming dominance of Chinese manufacturers is strengthening further. While global battery usage expanded steadily by 13.8 percent year-on-year, market leader CATL secured a share of over 40 percent. Together with second-place BYD, the two giants control more than half of the market. On the other hand, Japanese and South Korean manufacturers, who once led the market, are facing a difficult battle due to the slowdown in the European and US EV markets, which represent their primary customer base.

Global EV Battery Market Share January-April 2026 (Top 10)

According to data from market research firm SNE Research, the performance of the world’s major EV battery manufacturers is as follows. Total usage reached 352.7GWh, a 13.8 percent increase compared to the same period last year.

- 1st: CATL (China)

- Market Share: 40.1 percent

- Installed Capacity: 141.4GWh

- Year-on-Year Trend: 19.8 percent increase (Market share expansion)

- 2nd: BYD (China)

- Market Share: 14.2 percent

- Installed Capacity: 50.0GWh

- Year-on-Year Trend: 2.4 percent decrease (Slight share decline)

- 3rd: LG Energy Solution (South Korea)

- Market Share: 9.1 percent

- Installed Capacity: 32.0GWh

- Year-on-Year Trend: 8.3 percent increase (Slight share decline)

- 4th: CALB (China)

- Market Share: 5.1 percent

- Installed Capacity: 18.1GWh

- Year-on-Year Trend: 39.3 percent increase (Rapid growth)

- 5th: Gotion High-tech (China)

- Market Share: 4.4 percent

- Installed Capacity: 15.6GWh

- Year-on-Year Trend: 30.2 percent increase (Rapid growth)

- 6th: SK On (South Korea)

- Market Share: 3.5 percent

- Installed Capacity: 12.3GWh

- Year-on-Year Trend: 7.9 percent decrease (Share decline)

- 7th: Panasonic (Japan)

- Market Share: 3.4 percent

- Installed Capacity: 12.0GWh

- Year-on-Year Trend: 3.7 percent decrease (Share decline)

- 8th: Eve Energy (China)

- Market Share: 3.3 percent

- Installed Capacity: 11.5GWh

- Year-on-Year Trend: 30.3 percent increase

- 9th: Svolt Energy (China)

- Market Share: 2.6 percent

- Installed Capacity: 9.3GWh

- Year-on-Year Trend: 37.2 percent increase

- 10th: Sunwoda (China)

- Market Share: 2.5 percent

- Installed Capacity: 8.7GWh

- Year-on-Year Trend: 17.6 percent increase

- Others

- Market Share: 11.8 percent

- Installed Capacity: 41.7GWh

Key Topics from the Released Data

1. Overwhelming Dominance of Chinese Players (7 Companies in the Top 10)

Chinese companies took seven out of the top ten spots, with their combined share reaching 72.2 percent (an increase of 2.1 percentage points from the same period last year). In particular, the top two leaders, CATL (40.1 percent) and BYD (14.2 percent), alone account for 54.3 percent of the global market.

2. Stagnation and Decline of Major Japanese and South Korean Manufacturers

South Korea’s SK On (down 7.9 percent) and Japan’s Panasonic (down 3.7 percent) saw their installed capacities fall below the previous year’s levels. While South Korea’s top manufacturer, LG Energy Solution, increased its installed capacity, it could not keep pace with the growth rate of the overall market, resulting in a decline in market share.

Supplementary Context: For Deeper Understanding

This section explains the background context of why Chinese companies are so strong and why Japanese and South Korean companies are struggling.

Background on the Struggles of Japanese and South Korean Companies: “Slowing Western EV Markets” and the “Tesla Effect”

- Background of SK On (South Korea): The company took a direct hit from the temporary slowdown in EV sales growth (such as the EV chasm phenomenon) in North America and Europe, which are its primary customer bases.

- Background of Panasonic (Japan): Stagnant sales growth by its primary customer, Tesla, in specific regions directly resulted in a decrease in Panasonic’s battery installation capacity. Because Panasonic is highly dependent on Tesla, its business performance is structurally tied to its customer’s sales trends.

Why Chinese Companies Continue to Grow Rapidly: The Strength of “LFP Batteries”

- Chinese manufacturers (such as CATL, BYD, and CALB) possess a strong competitive advantage in producing low-cost LFP (lithium iron phosphate) batteries that do not use cobalt or nickel.

- Currently, “cost reduction” has become the most critical theme for surviving fierce competition in the global EV market. As a result, orders from automakers worldwide are concentrating on Chinese companies that can mass-supply cheap and safe LFP batteries, leading to a further expansion of their market share.

コメント