2026年3月1日現在のデータによると、人型ロボット(ヒューマノイド)市場は試験段階を脱し、爆発的な成長期に突入しています。特に中国メーカーが、米テスラなどの競合に先駆けて圧倒的な出荷台数を記録し、「独走」態勢を築いています。

市場の現状と予測(IDCデータ)

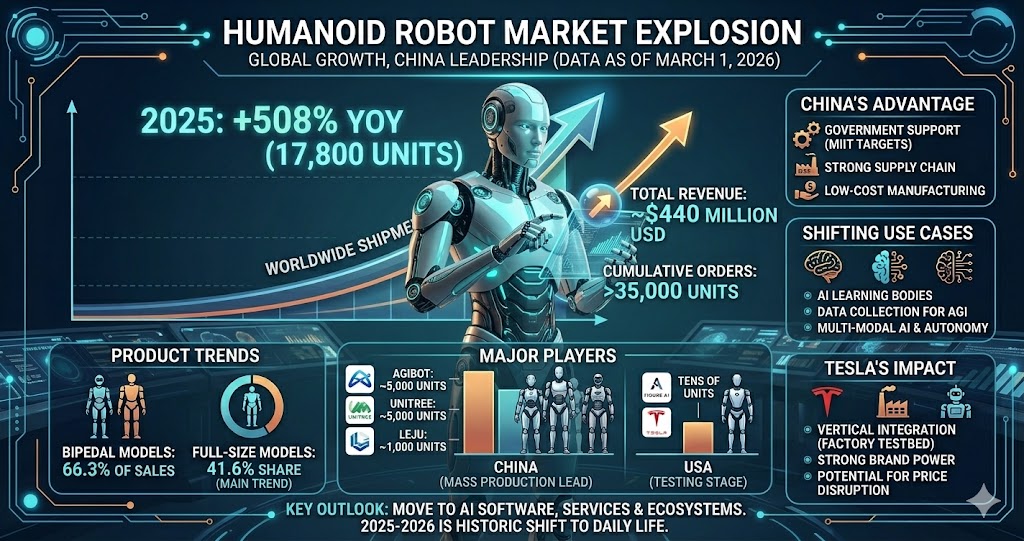

- 成長率: 2025年の世界出荷台数は前年比508%増の1万7800台に達する見通し。

- 経済規模: 売上高は約4億4000万ドル(約680億円)、累計受注は3万5000台を突破。

- 製品トレンド: 二足歩行型が売上の66.3%を占め、等身大の「フルサイズモデル」がシェア41.6%で主流となっています。

主要プレーヤーの勢力図

- 中国勢(量産先行):

- Agibot(智元機器人)、Unitree(宇樹科技): 出荷約5000台で業界を牽引。

- Leju(楽聚)、Booster(加速進化): 1000台規模を達成。

- その他: UBTECH、Galbot、Engine AIなどが数百台規模で追随。

- 米国勢(試験運用段階):

- Figure AI、Apptronik: 出荷は数十台にとどまる。

- Tesla(Optimus): 本格量産は2026年以降の予定。

関連情報と背景解説

このニュースを理解する上で重要な、3つの補足情報を付け加えます。

1. 中国が「独走」できる理由

中国が米国勢を圧倒している背景には、政府の強力な後押しとサプライチェーンの厚みがあります。

- 政策的支援: 中国工業情報化部(MIIT)は、2025年までに人型ロボットの量産体系を確立し、2027年までに世界のリーダーとなる目標を掲げています。

- コスト競争力: モーター、減速機、センサーなどの主要部品の多くを国内で低コストに調達できるため、1台あたりの価格を数万ドル(数百万円)程度まで抑えることに成功しています。

2. 活用シーンの変化:「AI学習の肉体」へ

これまでのロボットは「特定の作業」を行うためのものでしたが、現在は役割が変わってきています。

- データの収集: 人型ロボットを実際に動かし、人間と同じ環境で作業させることで、汎用AI(AGI)を訓練するための膨大なデータを取得しています。

- マルチモーダルAI: 最新モデルは視覚や触覚を統合したAIを搭載しており、指示がなくても周囲の状況を判断して動く「自律性」が高まっています。

3. テスラ「Optimus(オプティマス)」の影響力

現時点での出荷台数は中国勢が勝っていますが、業界全体がテスラの動向に注視しています。

- 垂直統合: テスラは自社のEV製造工場を「ロボットがロボットを作る」実証の場として活用できます。

- ブランド力: テスラが量産を開始すれば、一気に価格破壊が起きる可能性があるため、中国勢はそれまでに市場シェアを固めようと急いでいます。

今後の展望

今後は、単に「歩ける・動く」といったハードウェアの競争から、いかに複雑な作業をこなせるかという「AIソフトウェア」と、故障時にすぐ対応できる「サービスエコシステム」の構築へと競争の軸が移っていくでしょう。

ポイント: 2025年から2026年にかけては、人型ロボットが「SFの世界」から「工場や教育現場の日常」へと移り変わる歴史的な転換点となっています。

Chinese Manufacturers Take the Lead in Humanoid Robots: Surpassing Tesla with 17,000+ Global Shipments

According to data as of March 1, 2026, the humanoid robot market has moved beyond the pilot phase and entered a period of explosive growth. Chinese manufacturers, in particular, have achieved overwhelming shipment volumes ahead of competitors like Tesla, establishing a dominant “solo lead” in the industry.

Market Status and Forecast (IDC Data)

- Growth Rate: Global shipments for 2025 are projected to reach 17,800 units, a 508% increase year-on-year.

- Economic Scale: Revenue is estimated at approximately 440 million USD, with cumulative orders exceeding 35,000 units.

- Product Trends: Bipedal models account for 66.3% of sales, with life-sized “full-size models” becoming the mainstream, holding a 41.6% market share.

Competitive Landscape of Key Players

- Chinese Group (Leading in Mass Production):

- Agibot and Unitree Robotics: Leading the industry with approximately 5,000 units shipped.

- Leju Robotics and Booster Robotics: Achieved shipment scales of 1,000 units.

- Others: Companies like UBTECH Robotics, Galbot, and Engine AI are following with several hundred units each.

- US Group (Pilot/Testing Phase):

- Figure AI and Apptronik: Shipments remain limited to dozens of units.

- Tesla (Optimus): Full-scale mass production is not expected until 2026 or later.

Related Information and Contextual Commentary

Three key supplementary points are essential to understanding this news:

1. Why China is Taking the “Solo Lead”

China’s dominance over US competitors is backed by strong government support and a robust supply chain.

- Policy Support: China’s Ministry of Industry and Information Technology (MIIT) has set goals to establish a mass production system for humanoid robots by 2025 and to become a global leader by 2027.

- Cost Competitiveness: Many key components, such as motors, reducers, and sensors, can be sourced domestically at low cost. This has enabled manufacturers to successfully reduce the price per unit to tens of thousands of dollars.

2. Shifting Use Cases: Becoming the “Body for AI Learning”

While robots were previously designed for “specific tasks,” their roles are now evolving.

- Data Collection: By deploying humanoid robots in real-world environments, companies are acquiring vast amounts of data to train Artificial General Intelligence (AGI).

- Multimodal AI: Latest models feature AI that integrates vision and touch, increasing “autonomy” to navigate and act without specific instructions.

3. The Influence of Tesla’s “Optimus”

Despite China leading in current shipments, the entire industry remains focused on Tesla’s movements.

- Vertical Integration: Tesla can use its own EV manufacturing plants as a proving ground where “robots build robots.”

- Brand Power: Once Tesla begins mass production, it could trigger immediate price disruption. Chinese manufacturers are rushing to solidify their market share before this happens.

Future Outlook

The axis of competition is expected to shift from hardware—simply “walking and moving”—to “AI software” capable of complex tasks and the creation of “service ecosystems” for rapid maintenance and support.

Key Point: The period between 2025 and 2026 marks a historic turning point where humanoid robots transition from the world of science fiction to daily life in factories and educational settings.

コメント