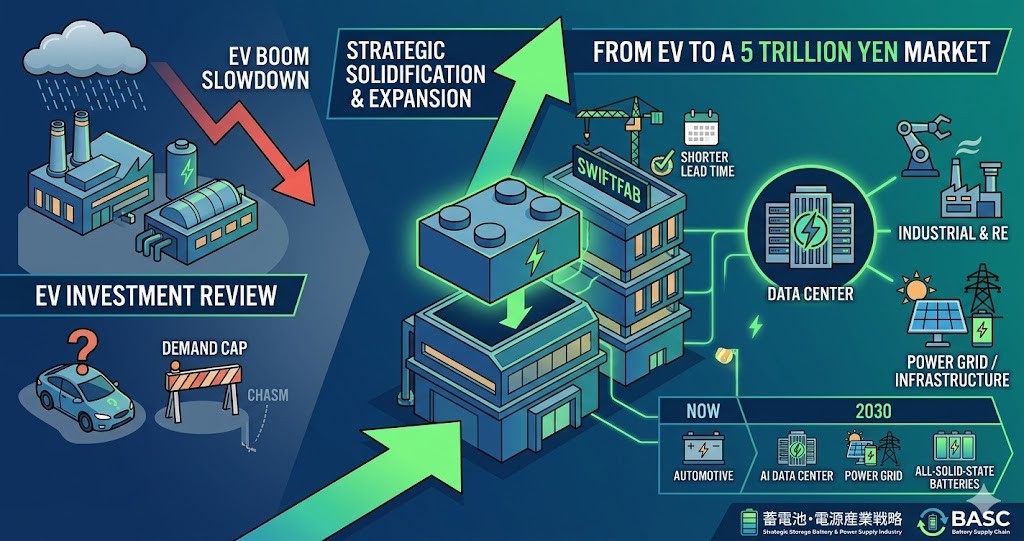

世界の自動車業界でEV(電気自動車)シフトの減速が指摘される中、日本の自動車大手が相次いで電池工場の投資計画を見直しています。一見すると後退のようにも映るこの動きですが、その実態は市場の急激な変化に対応するための「戦略的な足場固め」です。

経済産業省は2026年6月、従来の蓄電池産業戦略を改定し、AIデータセンターやインフラ領域を巻き込んだ新たな方針を発表しました。大量生産による「規模の経済」で圧倒する中国企業に対し、日本勢は技術力と柔軟性を武器に、自動車の枠を超えた5兆円市場へと舵を切ろうとしています。本稿では、ホンダや日産の計画見直しの背景と、日本産業界が描く次の一手についてまとめます。

- 1. ホンダ・日産などが電池工場計画を見直した理由

- 2. 経産省の新戦略:車載から「蓄電池・電源産業戦略」へ

- 3. 日本企業の戦い方:大量生産から「高付加価値」と「身軽さ」へ

- 4. 関連情報:世界のEV市場と蓄電池をめぐる補足

- まとめ

- 1. Why Honda, Nissan, and Others Are Reviewing Battery Factory Plans

- 2. METI’s New Strategy: Moving from Automotive to the “Battery and Power Supply Industry Strategy”

- 3. How Japanese Companies Fight: Shifting from Mass Production to “High Value” and “Agility”

- 4. Related Information: Supplementary Trends in the Global EV and Battery Markets

- Conclusion

1. ホンダ・日産などが電池工場計画を見直した理由

国内自動車各社がEV用電池工場の新設・稼働計画を凍結や先送り、あるいは撤回している背景には、大きく分けて3つの要因があります。

- 世界的なEV需要の伸び悩み(キャズムの到来) EV市場が初期の普及期から一般的な普及期に移行する中、一時的に需要の伸びが鈍化する「普及の谷間(キャズム)」に直面しています。先行きが不透明な中で巨額の固定費投資を急がず、需要を慎重に見極める姿勢にシフトしています。

- 中国企業による価格競争の激化と供給過剰 中国の電池メーカーが圧倒的な規模で大量生産を進めた結果、電池の市場価格は下落し続けています。現状の供給過剰のまま新工場を稼働させても、採算が合わないリスク(投資回収の困難さ)が高まっています。

- HV・PHVの好調による時間的猶予 日本勢は現在、世界的に需要が高まっているハイブリッド車(HV)やプラグインハイブリッド車(PHV)の販売が好調で、高い収益力を維持しています。この安定した業績が支えとなり、次世代の本命である「全固体電池」などの開発・投資へ資金を振り向ける時間的なゆとりが生まれています。

2. 経産省の新戦略:車載から「蓄電池・電源産業戦略」へ

経済産業省は2026年6月2日、これまでの「蓄電池産業戦略」を「蓄電池・電源産業戦略」へと改め、枠組みを大きく広げました。2035年に日本企業の関連売上高を現状の3倍となる約5兆円へ伸ばす目標を掲げています。

戦略の柱と数値目標

- 新領域(非車載)への拡大 生成AIの急速な普及に伴い、一瞬の停電も許されないAI向けデータセンターのバックアップ電源として大容量電池の需要が急増しています。また、再生可能エネルギーの出力安定化、ロボット、医療、防災、産業機械など、車載技術を応用できる高付加価値市場に焦点を当てます。

- 国内生産能力の引き上げ 国内の生産能力を、2030年から2030年代半ばまでに年間 150 GWh まで引き上げることを目指します。

- 次世代技術の確立 2030年ごろに全固体電池を実用化し、2030年代半ばには量産体制を整えます。

3. 日本企業の戦い方:大量生産から「高付加価値」と「身軽さ」へ

中国企業が「均一なものを一度にたくさん作る(多売)」のに対し、日本企業は「需要に合わせて上質なものを多品種少量で作る」という強みを生かした戦い方にシフトしています。

長寿命と緻密な制御

データセンターやインフラ向けには、突発的な大電力の充放電に耐える「タフさ」や、細やかな「電圧制御」が求められます。日本企業はこれまで培った品質の高さで勝負を進めます。

新たな製造手法「スイフトファブ」

投資リスクを抑えるため、ものづくりの仕組み自体も変革しています。電池サプライチェーン協議会(BASC)を契機に、日立製作所やリコーなど9社が共同事業体「スイフトファブエナジーシステムズ」を2025年12月に設立しました。

- 仕組み: 生産ラインをブロック(モジュール化)に小分けし、あらかじめ組み立ててから現場でつなぎ合わせる方式。

- 効果: 巨大工場への投資に比べ、設備費用を約7割削減。これまで2から3年かかっていた工場の立ち上げ期間を半分に短縮。

- 狙い: 固定費リスクを分散し、多品種少量生産や市場の急変動に身軽に対応。経済安全保障の観点から中国企業への販売は想定せず、国内および欧米・インドなどへの展開を目指します。

4. 関連情報:世界のEV市場と蓄電池をめぐる補足

本動向を理解する上で、世界の市場環境には以下のような関連トレンドが存在します。

- 欧米でのEV方針の見直し 欧州連合(EU)が2035年以降の内燃機関(エンジン)車新車販売の原則禁止方針を一部緩和(合成燃料の容認など)したほか、米国の環境規制の動向も流動的になっています。こうした政治・規制面での揺り戻しも、自動車メーカーがEV投資の速度をコントロールする要因となっています。

- 循環型ビジネス(リユース・リサイクル)の重要性 新戦略の根底には、車載用として役目を終えた電池を劣化度合いに応じてデータセンターや電力インフラの「据え置き型電池」として再利用する、サーキュラーエコノミー(循環型経済)の構築も含まれています。これにより、売り切り型ではない持続的な収益基盤が生み出されます。

まとめ

現在のホンダや日産の電池工場計画の見直しは、後ろ向きな撤退ではなく、中国の価格攻勢をかわしつつ、より勝算の高い市場へとリソースを再配置するための「戦略的転換」です。

自動車という枠を超え、データセンターや電力網といった国家のインフラの土台を支える存在へ。日本の蓄電池産業は、量的な拡大競争から、技術の融合による高付加価値な「循環型ビジネス」の確立へと、次の一歩を踏み出しています。

出典:https://merkmal-biz.jp/post/116202/2

From Automotive to Social Infrastructure: Honda and Nissan’s Investment Curbs and METI’s Blueprint for a 5 Trillion Yen Market

While a slowdown in the global shift toward electric vehicles (EVs) has been widely noted, major Japanese automakers are reviewing and adjusting their investment plans for battery factories one after another. Although this move might appear to be a step backward at first glance, it is actually a strategic consolidation of their footing to adapt to rapid market changes.

In June 2026, the Ministry of Economy, Trade and Industry (METI) revised its previous Battery Industry Strategy, unveiling a new policy that incorporates AI data centers and the broader infrastructure sector. In contrast to Chinese companies that dominate through economies of scale via mass production, Japanese players are leveraging their technological prowess and flexibility to pivot toward a 5 trillion yen market that extends far beyond the automotive sector. This article summarizes the background behind Honda and Nissan’s revised plans and outlines the next steps envisioned by Japanese industry.

1. Why Honda, Nissan, and Others Are Reviewing Battery Factory Plans

There are three main factors behind domestic automakers freezing, postponing, or canceling their plans to build and operate new EV battery factories:

- Slowing Global EV Demand (The Arrival of the Chasm) As the EV market transitions from the early adoption phase to mainstream adoption, it is facing a temporary slowdown in demand growth, known as the “chasm.” Amid this uncertainty, companies are shifting to a cautious stance to carefully gauge market demand rather than rushing into massive fixed-cost investments.

- Intensifying Price Competition and Oversupply by Chinese Firms Chinese battery manufacturers have engaged in mass production on an overwhelming scale, causing market prices for batteries to fall continuously. Operating new factories under the current conditions of oversupply poses a high risk of unprofitability, making it difficult to recover investments.

- Breathing Room Courtesy of Strong HEV and PHEV Sales Japanese automakers are currently maintaining robust profitability due to strong global sales of hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs). This stable financial performance gives them the breathing room and flexibility to redirect funds toward developing and investing in next-generation solutions like all-solid-state batteries.

2. METI’s New Strategy: Moving from Automotive to the “Battery and Power Supply Industry Strategy”

On June 2, 2026, METI modified its former “Battery Industry Strategy” into the “Battery and Power Supply Industry Strategy,” significantly broadening its scope. The ministry has set a target to triple the related sales of Japanese companies to approximately 5 trillion yen by 2035.

Strategic Pillars and Numerical Targets

- Expansion into New (Non-Automotive) Sectors With the rapid spread of generative AI, demand for large-capacity batteries has surged for use as backup power sources in AI data centers, where even a momentary power outage is unacceptable. The strategy focuses on high-value-added markets where automotive battery technology can be applied, such as stabilizing renewable energy output, robotics, medical care, disaster prevention, and industrial machinery.

- Boosting Domestic Production Capacity The goal is to increase domestic production capacity to 150 GWh per year between 2030 and the mid-2030s.

- Establishing Next-Generation Technology The strategy aims to commercialize all-solid-state batteries around 2030 and establish a mass-production system by the mid-2030s.

3. How Japanese Companies Fight: Shifting from Mass Production to “High Value” and “Agility”

While Chinese companies focus on high-volume sales of uniform products, Japanese companies are shifting to a strategy that plays to their strengths: high-mix, low-volume production of premium items tailored to specific customer needs.

Long Lifespan and Precise Control

Data centers and infrastructure applications require exceptional durability to withstand sudden, heavy power charging and discharging, as well as meticulous voltage control. Japanese companies are moving forward by competing on the high quality they have cultivated over the years.

“Swift Fab”: A Revolutionary Manufacturing Method

To mitigate investment risks, companies are also transforming the very structure of manufacturing. Triggered by activities within the Battery Supply Chain Association (BASC), nine companies—including Hitachi and Ricoh—established a joint venture called “Swift Fab Energy Systems” in December 2025.

- Mechanism: The production line is divided into small blocks (modularized), pre-assembled, and then easily connected at the customer’s site.

- Effect: Reduces equipment costs by approximately 70 percent compared to investing in conventional mega-factories. It also cuts factory startup times—which previously took 2 to 3 years—in half.

- Objective: Distributes fixed-cost risks and creates an agile manufacturing environment capable of flexibly handling high-mix, low-volume production and sudden market fluctuations. From an economic security standpoint, sales to Chinese companies are not envisioned, as the venture aims to expand domestically as well as into Europe, the US, and India.

4. Related Information: Supplementary Trends in the Global EV and Battery Markets

To better understand these developments, the following related trends in the global market environment are worth noting:

- Revisions to EV Policies in Europe and the US The European Union (EU) has partially eased its plan to ban the sale of new internal combustion engine (ICE) vehicles by 2035 (such as by allowing synthetic fuels), and environmental regulations in the US remain fluid. These political and regulatory shifts are another key reason why automakers are controlling the pace of their EV investments.

- The Importance of Circular Business Models (Reuse and Recycling) At the core of the new strategy is the creation of a circular economy. Batteries that have reached the end of their automotive lifespan will be reused as stationary batteries for data centers and power infrastructure based on their degradation levels. This generates a sustainable revenue base that moves away from a simple, one-time sales model.

Conclusion

The current adjustments to battery factory plans by Honda and Nissan are not a backward retreat, but rather a strategic pivot designed to dodge China’s aggressive price competition while reallocating resources to markets with a higher probability of success.

By transcending the boundaries of the automotive industry, these companies are transforming into essential providers that anchor national infrastructure, such as data centers and power grids. The Japanese battery industry is taking its next step forward, moving away from a quantitative volume race and toward establishing a high-value-added “circular business” through the integration of technologies.

コメント