中国のエネルギー貯蔵(ストレージ)市場では、リチウムイオン電池に代わる低コストな選択肢として「ナトリウムイオン電池」の実用化が急速に進んでいます。2026年現在、業界の関心は「いかにエネルギー密度を高めるか」から「いかに安く、長く使えるか」へと移行しており、それに伴い電池の心臓部である正極材のトレンドも大きな転換点を迎えています。

以下に、最新の市場動向と技術的な背景をまとめました。

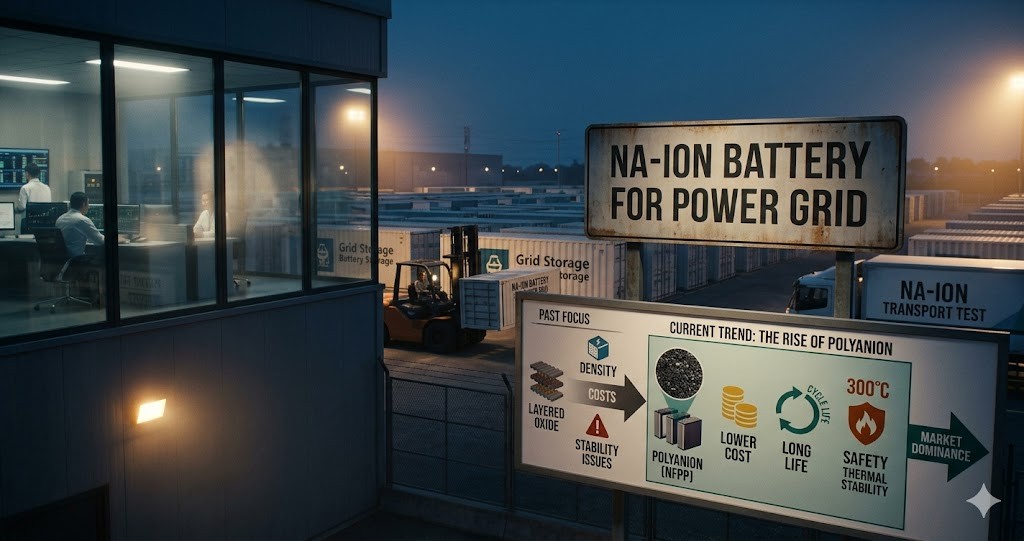

1. 正極材の主流が「ポリアニオン系」へシフト

中国のナトリウムイオン電池産業では、正極材料の選択において明確な構造変化が起きています。これまで主流の一つだった「層状酸化物」に代わり、ポリアニオン系(主にNFPP:フッ化リン酸バナジウムナトリウムなど)が台頭しています。

- 市場シェアの拡大: 2026年にはポリアニオン系材料が生産シェアの大部分を占める見込みで、特定の報告期間では70%を超える圧倒的なシェアを記録しています。

- エネルギー貯蔵への特化: 中国での主な用途はグリッドストレージ(系統用蓄電池)です。この分野では、瞬間的なパワーよりも「長寿命(サイクル特性)」「低コスト」「安全性」が重視されるため、構造的に安定したポリアニオン系が選好されています。

2. 層状酸化物が直面する課題

かつて期待された層状酸化物ルートは、現在、構造的な圧力にさらされています。

- コストと安定性の問題: 高価な遷移金属を必要とし、製造プロセスも複雑なため、大規模な蓄電システムではコスト競争力が維持しにくくなっています。

- 用途の限定化: 充放電を繰り返す際の構造劣化が課題となり、現在はエネルギー密度を優先する小型モビリティや、初期段階の実証実験といったニッチな用途への採用に留まっています。

3. 安全性の飛躍的向上と実用化試験

技術検証段階から産業規模の生産へ移行する中で、安全性と実用性の証明が進んでいます。

- 極限環境での耐性: 実験室での試験では、300℃という高温にさらされても熱暴走を起こさない高い熱安定性が確認されました。

- 商用車での試験: 大型トラックなどの輸送車両を用いた商業試験が実施されており、実際の運用条件下で走行距離や運転効率の向上が実証されています。

- 不燃性電解質の導入: 故障時のリスクを最小限に抑えるため、不燃性電解質を組み合わせたシステム設計も検討されています。

4. 今後の展望:用途に応じた「使い分け」の時代へ

今後のナトリウムイオン電池市場は、一つの材料が全てを支配するのではなく、用途に応じて最適化された複数のルートが共存する構造になると予想されます。

| 材料系統 | 主な用途・特徴 |

| ポリアニオン系 (NFPP) | 主流。エネルギー貯蔵(ESS)、長寿命、高安全性。 |

| 層状酸化物 | 高エネルギー密度が必要な用途、特定のモバイル機器。 |

| プルシアンブルー類似体 | 急速充電が必要なシナリオ、特定のニッチ市場。 |

まとめ

中国におけるナトリウムイオン電池は、2026年を通じて生産能力を拡大し続けています。リチウムイオン電池を完全に置き換えるのではなく、コストと安全性が最優先されるエネルギー貯蔵分野を中心に、独自の市場を確立しつつあります。技術の焦点が「理論上の性能」から「1サイクルあたりのコスト(LCOS)」へと移ったことが、現在のポリアニオン系へのシフトを決定づけています。

関連情報:なぜ今ナトリウムなのか?

ナトリウムは塩の主成分であり、地球上に広く豊富に存在するため、リチウムのように地政学的な供給リスクや価格高騰の影響を受けにくいという利点があります。リチウムイオン電池(LIB)の価格が下落した際にも、資源の自給率向上という観点から、中国政府や企業は戦略的にナトリウム技術の投資を継続しています。

From Layered Oxides to Polyanions: Structural Shifts in China’s Sodium-ion Battery Industry

In China’s energy storage market, the commercialization of Sodium-ion batteries is rapidly advancing as a low-cost alternative to Lithium-ion batteries. As of 2026, industry focus has shifted from “maximizing energy density” to “minimizing cost and maximizing longevity.” Consequently, the trends for cathode materials—the core of the battery—are reaching a major turning point.

The following is a summary of the latest market trends and technical backgrounds.

1. Mainstream Cathode Materials Shift to “Polyanion-based” Systems

A clear structural change is occurring in the selection of cathode materials within China’s Sodium-ion battery industry. Polyanion-based systems (primarily NFPP: Sodium Vanadium Fluorophosphate) are rising to replace “Layered Oxides,” which were previously a dominant path.

- Expansion of Market Share: Polyanion materials are expected to account for the majority of production share in 2026, recording an overwhelming share of over 70% in specific reporting periods.

- Specialization in Energy Storage: The primary application in China remains grid storage. In this sector, “long cycle life,” “cost stability,” and “safety” are prioritized over instantaneous power, leading to a preference for structurally stable polyanion systems.

2. Challenges Facing Layered Oxides

The layered oxide route, once highly anticipated, is now facing significant structural pressure.

- Cost and Stability Issues: Due to the requirement for expensive transition metals and complex manufacturing processes, it is difficult to maintain cost competitiveness in large-scale storage systems.

- Limited Applications: Structural degradation during repeated charge-discharge cycles remains a challenge. Currently, its use is limited to niche applications such as small-scale mobility where energy density is prioritized, or early-stage demonstration projects.

3. Breakthroughs in Safety and Practical Trials

As the industry transitions from technical verification to industrial-scale production, proof of safety and utility is advancing.

- Extreme Environment Resistance: Laboratory tests have confirmed high thermal stability, with batteries surviving temperatures up to 300 degrees C without entering thermal runaway.

- Commercial Vehicle Trials: Commercial trials using transport vehicles like heavy-duty trucks are underway, demonstrating improved operating efficiency and range under real-world conditions.

- Non-flammable Electrolytes: System-level designs using non-flammable electrolytes are being explored to further enhance safety margins during failure.

4. Outlook: An Era of Application-Specific Solutions

The future Sodium-ion battery market is expected to be a landscape where multiple optimized routes coexist rather than a single material dominating the entire field.

| Material System | Primary Applications and Features |

| Polyanion (NFPP) | Mainstream. Energy Storage (ESS), long life, high safety. |

| Layered Oxides | Applications requiring high energy density, specific mobile devices. |

| Prussian Blue Analogs | Fast-charging scenarios, specific niche markets. |

Summary

Throughout 2026, China’s Sodium-ion battery production capacity continues to expand. Rather than completely replacing Lithium-ion batteries, Sodium-ion technology is establishing its own market, centered on the energy storage sector where cost and safety are the top priorities. The shift to polyanion systems is driven by the industry’s focus moving from “theoretical performance” to “Levelized Cost of Storage (LCOS).”

Related Information: Why Sodium Now?

Sodium is the primary component of salt and is abundantly available worldwide. This makes it less susceptible to the geopolitical supply risks and price volatility associated with lithium, ensuring a stable supply chain for the future of energy.

コメント