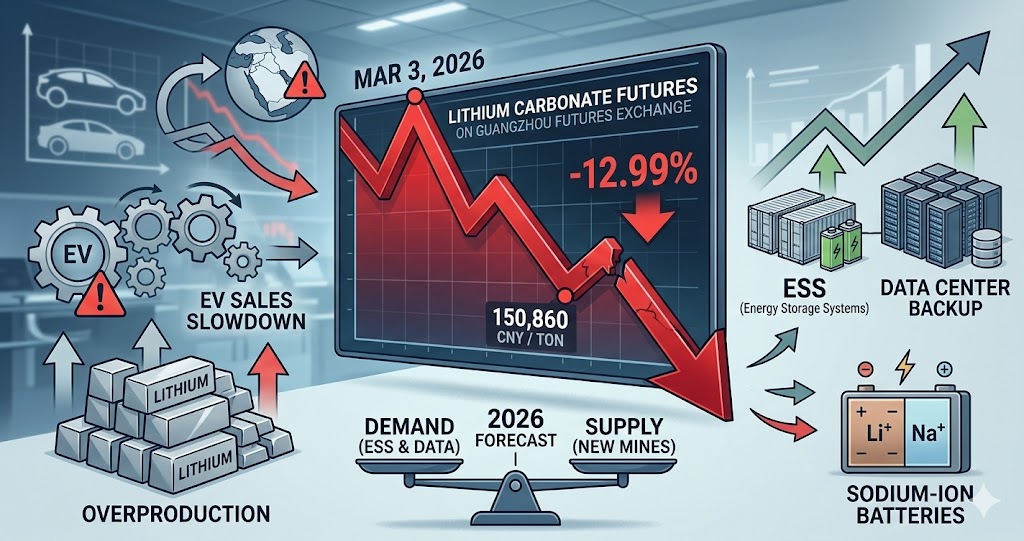

2026年3月3日、中国の広州先物取引所において、炭酸リチウム先物価格が前日比12.99%下落し、1トン当たり15万860元で取引を終えました。これは1日の値幅制限(13%)に近い大幅な下落です。

急落の主な要因

- EV販売の失速: 大手EVメーカーの販売低迷に加え、税制優遇措置の段階的廃止による需要減退への懸念。

- 中東情勢の緊迫化: 地政学リスクの拡大が世界経済の見通しを不透明にし、需要予測を悪化させた。

- 供給過剰の懸念: 2026年には供給が前年比19%から34%増加すると予測されており、需給バランスの緩和が意識された。

関連情報:リチウム市場の「変質」と新たな需要源

市場では現在、EV向け需要の鈍化を補う「新たな柱」として、電力貯蔵システム(ESS)とデータセンターが注目されています。

1. エネルギー貯蔵システム(ESS)が「ゲームチェンジャー」に

EV向けが停滞する一方で、電力網の安定化や再生可能エネルギーの貯蔵用バッテリー需要が急増しています。

- 需要シフト: 2026年には総需要の約31%をエネルギー貯蔵向けが占めると予測されています(2025年は23%)。

- データセンター需要: 世界的なデータセンター建設ブームに伴い、バックアップ電源としてのリチウム電池需要が予想を上回るペースで拡大しています。

2. 次世代技術「ナトリウムイオン電池」の台頭

リチウム価格の変動リスクを避けるため、より安価で資源豊富なナトリウムを用いた電池への移行が加速しています。

- CATLの動向: 中国の電池最大手CATLは、2026年からナトリウムイオン電池の本格導入を開始する計画です。

- コストメリット: ナトリウムイオン電池は、リチウムイオン電池(LFP)と比較して材料コストを20%から40%削減できる可能性があります。

市場予測:2026年の需給と価格見通し

アナリストによる予測は、供給過剰と不足の間で揺れています。

| 指標 | 2026年の予測値・推移 |

| リチウム需要成長率 | 前年比 +17% から +30% |

| リチウム供給成長率 | 前年比 +19% から +34% |

| 予測価格帯 | 1トン当たり 8万 から 20万 元 (11,432 – 28,580 USD) |

| 需給バランス | モルガン・スタンレー:8万トンの不足 / UBS:2.2万トンの不足 |

今後の注目点

今後は、リチウム価格が「エネルギー貯蔵の経済性」を維持できる水準(高すぎず安すぎず)で安定するかが焦点となります。価格が高すぎればナトリウムイオン電池への転換が加速し、安すぎればリチウム鉱山の生産抑制が再び始まると予想されます。

China Lithium Prices Plunge Nearly 13%: EV Slump and Geopolitical Risks Hit Demand

On March 3, 2026, lithium carbonate futures on the Guangzhou Futures Exchange plummeted by 12.99% from the previous day, closing at 150,860 yuan per tonne. This significant drop brought prices close to the daily limit of 13%.

Primary Factors for the Sharp Decline

- Slowing EV Sales: In addition to sluggish sales from major EV manufacturers, there are growing concerns over declining demand following the gradual phase-out of tax incentives.

- Escalating Tensions in the Middle East: Expanding geopolitical risks have clouded the outlook for the global economy, leading to a deterioration in demand forecasts.

- Oversupply Concerns: Global supply is projected to increase by 19% to 34% year-on-year in 2026, leading the market to anticipate a significant easing of the supply-demand balance.

Related Information: The “Structural Shift” in the Lithium Market

The market is currently pivoting toward Energy Storage Systems (ESS) and data centers as “new pillars” to compensate for the slowdown in EV-related demand.

1. Energy Storage Systems (ESS) as a “Game Changer”

While EV demand remains stagnant, there is a surge in demand for batteries used in power grid stabilization and renewable energy storage.

- Demand Shift: It is predicted that energy storage will account for approximately 31% of total lithium demand in 2026 (up from 23% in 2025).

- Data Center Demand: The global construction boom in data centers is driving lithium battery demand for backup power systems at a faster-than-expected pace.

2. Rise of Next-Generation “Sodium-Ion Battery” Technology

To hedge against the volatility of lithium prices, the industry is accelerating the shift toward sodium-based batteries, which utilize cheaper and more abundant materials.

- CATL’s Move: CATL, China’s battery giant, plans to begin the full-scale implementation of sodium-ion batteries starting in 2026.

- Cost Advantages: Sodium-ion batteries have the potential to reduce material costs by 20% to 40% compared to lithium-ion (LFP) batteries.

Market Forecast: 2026 Supply-Demand and Price Outlook

Analyst forecasts remain divided between potential oversupply and shortages.

| Indicator | 2026 Forecast / Trend |

| Lithium Demand Growth Rate | +17% to +30% Year-on-Year |

| Lithium Supply Growth Rate | +19% to +34% Year-on-Year |

| Projected Price Range | 80,000 to 200,000 yuan per tonne (11,432 – 28,580 USD) |

| Supply-Demand Balance | Morgan Stanley: 80,000-tonne deficit / UBS: 22,000-tonne deficit |

Future Outlook

The key focus moving forward will be whether lithium prices stabilize at a level that maintains the “economic viability of energy storage”—neither too high nor too low. If prices remain too high, the transition to sodium-ion batteries will accelerate. If they drop too low, it is expected that lithium mines will once again begin curbing production.

コメント