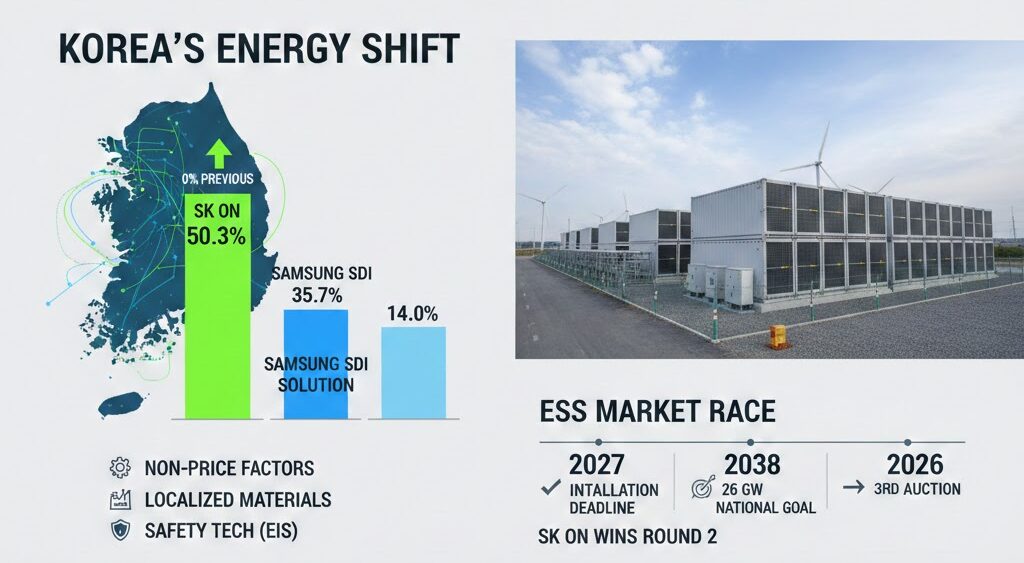

韓国政府(気候・エネルギー・環境省および韓国電力取引所)が実施した第2回「系統用ESS中央契約市場」の入札結果が発表され、前回(第1回)は落札ゼロだったSKオンが、全体の50.3%を確保して首位に立ちました。

1. 入札結果の概要(第2回)

今回の入札は、全羅南道と済州島の計7地点に設置される合計 565 MW (メガワット) のプロジェクトを対象としています。

| 企業名 | 落札容量 | シェア(前回比) |

| SKオン | 284 MW | 50.3% (前回 0%) |

| サムスンSDI | 202 MW | 35.7% (前回 76%) |

| LGエナジーソリューション | 79 MW | 14.0% (前回 24%) |

2. SKオンが逆転勝利した要因

業界関係者は、SKオンの勝利の背景に以下の戦略があったと分析しています。

- 非価格要素の強化: 今回の審査では「産業・経済への貢献」や「安全性」といった非価格要素の比率が引き上げられました。

- 材料の国産化コミット: 負極材、電解液、セパレーターなどの主要材料を韓国国内サプライヤーから調達する計画を提示し、国内エコシステムへの貢献が高く評価されました。

- 安全性技術の導入: 韓国メーカーとして初めて、火災の兆候を30分前に検知できる「電気化学インピーダンス分光法(EIS)」ベースの診断システムを採用しました。

3. 【関連情報】背景と今後の市場戦略

- LFP(リン酸鉄リチウム)電池へのシフト: 中国勢(CATLなど)が圧倒的シェアを持つESS市場に対し、韓国勢も安価で安全性の高いLFP電池で対抗を強めています。SKオンは瑞山第2工場に 3 GWh (ギガワット時) のLFP専用ラインを設置予定で、今後は 6 GWh への拡張も検討しています。

- 「キャズム(普及の停滞)」対策: 電気自動車(EV)市場の成長が一時的に鈍化する中、バッテリー各社は成長が続くESS(電力網向け貯蔵装置)を新たな収益の柱として重視しています。

- 政府の目標: 韓国政府は、再生可能エネルギーの拡大に伴う電力網の安定化のため、2038年までに合計 26 GW (26,000 MW) 規模のESSを導入する長期計画を掲げています。

今後の展望

今回の落札者は、2027年12月までに施設の設置を完了させる必要があります。また、2026年後半には第3回の入札が予定されており、今回の結果を受けてサムスンSDIやLGエナジーソリューションがどのような対抗策を打ち出すかが注目されます。

注記: 第2回入札の総事業規模は約1兆ウォン(約6億9530万ドル / 約1040億円)に達します。

出典:https://www.koreaherald.com/article/10675903

SK On Secures Over 50% in Korean Government ESS Tender: A Dramatic Reversal from Zero to Market Leader

The results for the second “Centralized ESS Contract Market” tender, conducted by the South Korean government (Ministry of Climate, Energy and Environment and Korea Power Exchange), have been announced. SK On, which secured zero bids in the first round, has now taken the lead by capturing 50.3% of the total capacity.

1. Summary of the Second Tender Results

This tender covers projects totaling 565 MW (megawatts) to be installed across seven locations in South Jeolla Province and Jeju Island.

| Company Name | Awarded Capacity | Share (vs Previous Round) |

| SK On | 284 MW | 50.3% (Previously 0%) |

| Samsung SDI | 202 MW | 35.7% (Previously 76%) |

| LG Energy Solution | 79 MW | 14.0% (Previously 24%) |

2. Factors Behind SK On’s Comeback Victory

Industry experts analyze that the following strategies were key to SK On’s success:

- Strengthening Non-Price Factors: In this evaluation, the weighting of non-price factors, such as “contribution to industry and economy” and “safety,” was increased.

- Commitment to Domestic Materials: SK On proposed a plan to procure key materials—including cathodes, electrolytes, and separators—from South Korean domestic suppliers, receiving high marks for contributing to the local ecosystem.

- Implementation of Safety Technology: SK On became the first Korean manufacturer to adopt a diagnostic system based on “Electrochemical Impedance Spectroscopy (EIS),” which can detect signs of fire up to 30 minutes in advance.

3. Related Information: Background and Market Strategy

- Shift to LFP (Lithium Iron Phosphate) Batteries: To compete in an ESS market dominated by Chinese companies like CATL, Korean firms are strengthening their lineup of cost-effective and safe LFP batteries. SK On plans to install a 3 GWh (gigawatt-hour) dedicated LFP line at its Seosan Second Plant, with considerations to expand to 6 GWh in the future.

- Addressing the “EV Chasm”: As growth in the Electric Vehicle (EV) market temporarily slows down, battery manufacturers are prioritizing the steadily growing ESS (Grid Energy Storage) sector as a new revenue pillar.

- Government Goals: To stabilize the power grid amid the expansion of renewable energy, the South Korean government has set a long-term plan to install a total of 26 GW (26,000 MW) of ESS capacity by 2038.

Future Outlook

The winners of this bid must complete the installation of facilities by December 2027. A third round of bidding is scheduled for late 2026. Attention is now focused on how Samsung SDI and LG Energy Solution will respond to recover their positions in the next round.

Note: The total project scale for the second tender reaches approximately 1 trillion won (roughly 695.3 million US dollars).

コメント