2025年は、蓄電池市場にとって「需給バランスの劇的な逆転」と「脱・中国一極集中」が鮮明になった歴史的な転換点です。

1. 市場規模と需給バランスの変遷

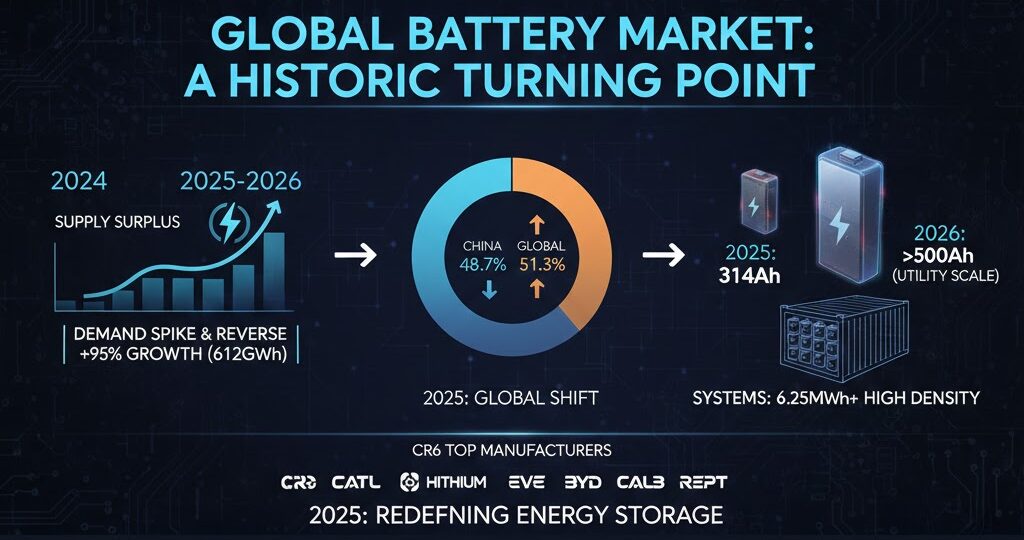

2025年の出荷量は前年比約95%増の612.39GWhと急膨張しました。

- 需給の逆転: 2024年までの供給過剰から一転し、2025年第2〜3四半期には需給逼迫へ移行しました。これによりセル価格の下落に歯止めがかかり、コスト上昇分が下流(システム側)へ転嫁される局面に入っています。

- 2026年の展望: 出荷量は801GWhまで拡大する見込みです。上半期は逼迫が続きますが、下半期には新工場の稼働などにより緩やかに緩和すると予測されています。

2. 技術トレンド:大容量化の加速(Ah競争)

ユーティリティスケール(事業用)を中心に、セルの大容量化によるLCOS(均等化蓄電コスト)の低減が至上命題となっています。

| カテゴリ | 2025年の主力 | 2026年の予測・トレンド |

| 事業用セル | 314Ahが主流化 | 500Ah超(587Ah/588Ah等)へ移行。2026年には浸透率15%超へ。 |

| 住宅用セル | 100Ahからの移行期 | 314Ahへの移行が加速。2026年には普及率20%に迫る。 |

| システム | 4MWhクラス | 6.25MWh+(20ftコンテナ)など、さらなる高密度化。 |

3. グローバル競争とシェアの地殻変動

中国メーカーの圧倒的優位は揺るがないものの、市場の構成比とプレイヤーの顔ぶれに変化が生じています。

- 中国国外市場の逆転: 2025年下半期、中国以外の市場向け出荷(51.3%)が初めて中国国内向けを上回りました。 米国のIRA法による補助金や、欧州・新興国(豪州・中東)での再エネ併設需要が牽引しています。

- トップ集団の固定化と追撃: * CR6(上位6社): CATL、Hithium、EVE Energy、BYD、CALB、REPT BATTERO。この6社で市場の約75%を占めます。

- 韓国勢の苦戦: Samsung SDIやLG Energy Solutionがトップ10から脱落(海外向けではLGが9位に踏みとどまる)。LFP(リン酸鉄リチウム)へのシフト遅れが響いています。

- 中堅層の台頭: 上位10社の集中度(CR10)が90%を下回ったことは、2番手・3番手グループの供給能力が向上し、システムインテグレーターが調達先を多様化させている証拠です。

補足:なぜ「中国以外」が伸びているのか?

- AI・データセンター需要: 北米を中心にAIインフラ向けのバックアップ電源として蓄電池需要が爆発しています。

- 電力価格のボラティリティ: 欧州や豪州では市場価格に連動した裁定取引(安い時に貯め、高い時に売る)の収益性が向上し、補助金なしでの導入が進んでいます。

- 長時間蓄電(LDES)への移行: 従来の2時間から4〜8時間の長時間蓄電プロジェクトが増加しており、1プロジェクトあたりの容量が大型化しています。

From Oversupply to “Tightness”: A Historic Turning Point for the Battery Cell Market and the 2026 Outlook

The year 2025 marks a historic turning point for the energy storage market, characterized by a “dramatic reversal in supply-demand balance” and a clear shift toward “de-concentration from China.”

1. Market Scale and Supply-Demand Dynamics

Global shipments in 2025 skyrocketed to 612.39 GWh, a year-on-year increase of approximately 95%.

- Supply-Demand Reversal: Pivoting from the oversupply of 2024, the market shifted to a supply shortage between Q2 and Q3 of 2025. This halted the decline in cell prices, leading to a phase where increased costs are being passed down to downstream system integrators.

- 2026 Outlook: Shipments are projected to expand to 801 GWh. While tightness is expected to persist through the first half of the year, it is forecast to ease gradually in the second half as new production facilities come online.

2. Tech Trends: Acceleration of Large-Capacity Cells (The “Ah” Race)

Reducing the Levelized Cost of Storage (LCOS) through larger cell capacities has become a top priority, particularly for utility-scale applications.

| Category | 2025 Mainstream | 2026 Forecast & Trends |

| Utility-Scale Cells | 314Ah becomes the standard. | Transition to 500Ah+ (587Ah/588Ah). Penetration to exceed 15% in 2026. |

| Residential Cells | Transitioning from 100Ah. | Acceleration toward 314Ah. Penetration likely to approach 20% in 2026. |

| Systems | 4MWh class. | Further densification to 6.25MWh+ (within 20ft containers). |

3. Global Competition and Shifting Market Shares

While Chinese manufacturers maintain a dominant lead, the market composition and key players are evolving.

- Inversion of Non-China Markets: In the second half of 2025, shipments to markets outside of China reached 51.3%, surpassing China’s domestic shipments for the first time. This is driven by US IRA subsidies and renewable energy integration in Europe and emerging markets (Australia/Middle East).

- Top-Tier Dominance vs. New Contenders:

- CR6 (Top 6): CATL, Hithium, EVE Energy, BYD, CALB, and REPT BATTERO account for nearly 75% of the market.

- South Korean Manufacturers’ Struggle: Samsung SDI and LG Energy Solution fell out of the global top 10 (though LG remains 9th in the non-China ranking). This is largely due to a delay in shifting to LFP (Lithium Iron Phosphate) chemistry.

- Rise of Tier 2 & 3 Suppliers: The fact that the top 10 concentration (CR10) fell below 90% indicates strengthening momentum from secondary suppliers and a move by system integrators to diversify their supply chains.

Appendix: Why is the “Non-China” Market Growing?

- AI & Data Center Demand: Especially in North America, demand for energy storage as backup power for AI infrastructure is exploding.

- Electricity Price Volatility: In Europe and Australia, the profitability of arbitrage (buying low, selling high) linked to market prices is rising, driving installations even without subsidies.

- Shift to Long-Duration Energy Storage (LDES): A move from traditional 2-hour storage to 4–8 hour projects is increasing the capacity required per project.

コメント