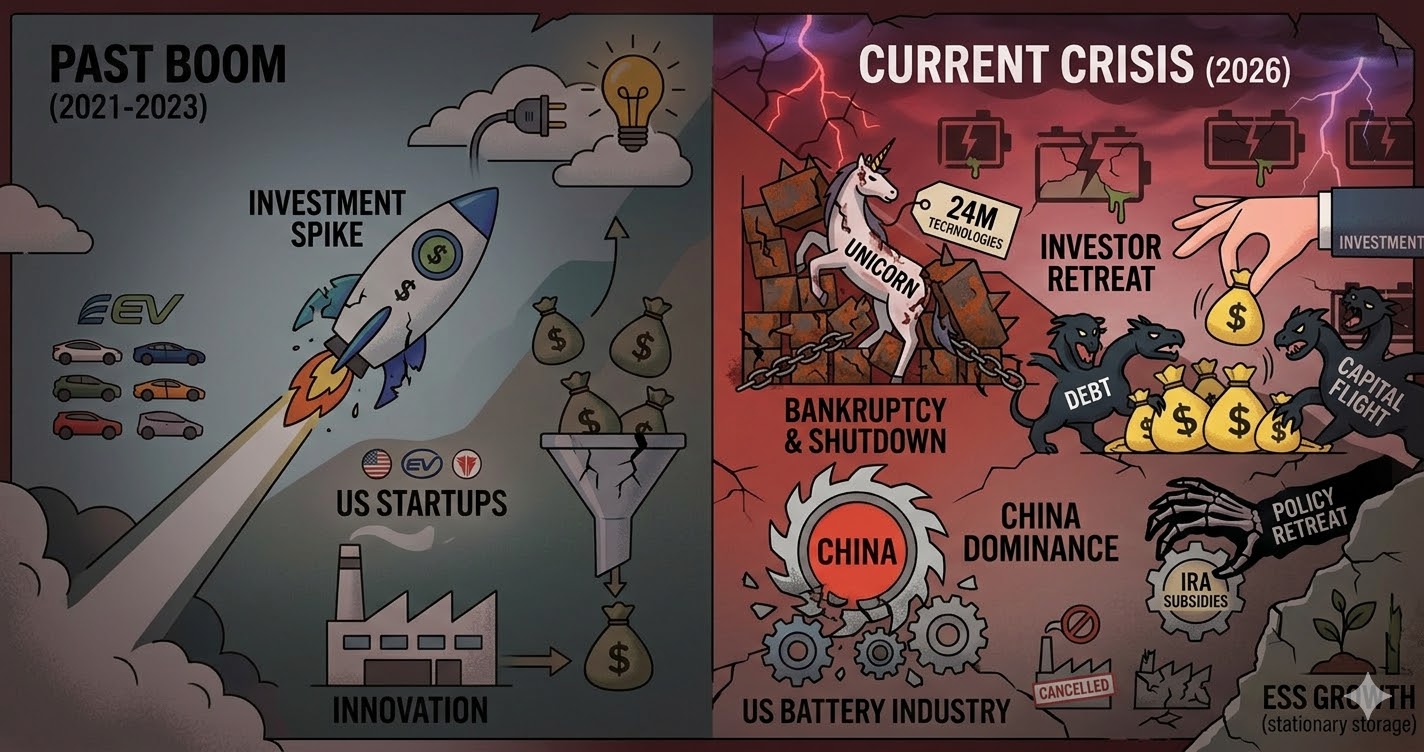

2020年代前半の投資ブームから一転し、2026年現在の米国電池業界は、有力スタートアップの倒産や投資撤退が相次ぐ厳しい局面に立たされています。

1. 象徴的な企業の崩壊:24M Technologiesの事例

かつて企業価値10億ドル(ユニコーン企業)を超えていた24M Technologiesの閉鎖は、業界に大きな衝撃を与えています。

- 革新性: 従来のリチウムイオン電池の製造プロセスを簡略化し、厚い電極層によってエネルギー密度を高める技術を保有。航続距離1000マイル(約1600キロメートル)の実現を目標としていました。

- 挫折の背景: 同社の技術は既存の化学組成に適合しやすく、比較的「実現可能性が高い」と目されていましたが、量産化や資金維持の壁を越えられず、資産競売に至りました。

2. 相次ぐスタートアップの脱落

24M以外にも、期待されていた有力企業が事業停止や破産に追い込まれています。

- Natron Energy: 米国を代表するナトリウムイオン電池の旗手でしたが、2025年9月に事業停止。

- Ample: EVの電池交換システムを展開していましたが、2025年12月に破産申請。

- 投資環境の変化: ベンチャーキャピタルによる「イノベーションへの意欲」が減退し、新規の斬新なアイデアへの資金供給が滞っています。

3. 停滞を招いた複合的要因

米国の電池エコシステムを支えていた前提条件が崩れつつあります。

- 政策の後退: インフレ抑制法(IRA)による補助金や優遇措置が骨抜きにされたことで、投資的魅力が激減しました。

- EV市場の冷え込み: 消費者の需要減速を受け、自動車メーカーはEV開発の中止や工場建設の縮小を余儀なくされています。

- 中国勢の支配: 米国が苦戦する一方で、中国の電池・EVメーカーは圧倒的なサプライチェーンとコスト競争力を武器に、世界市場での支配力をさらに強めています。

4. 残された「明るい兆し」

厳しい状況下でも、一部の領域では成長の可能性が残っています。

- 定置型エネルギー貯蔵(ESS): EV向けは苦戦していますが、電力網向けの蓄電システム市場は米国を含め依然として成長傾向にあります。

- 製造プロセスの改善: 24Mが目指したような「コスト削減に直結する製造技術」の重要性は、生き残った企業の間で引き続き高く評価されています。

比較まとめ:電池業界の「成功」と「失敗」の分岐点

| 項目 | 過去のブーム期 (2021-2023) | 現在の停滞期 (2026) |

| 資金調達 | 巨額資金が未検証の技術にも流入 | 投資家は保守的になり、資金引き揚げが加速 |

| 主要ターゲット | 長距離EV、新型化学技術(全固体など) | ESS(定置型蓄電)、既存技術のコスト削減 |

| 政策環境 | IRAによる強力な後押し | 法案の骨抜きによる支援策の不透明化 |

| 市場の主役 | 米国スタートアップの乱立 | 中国大手企業による支配的地位の確立 |

出典:https://www.technologyreview.com/2026/03/12/1134197/us-battery-industry/

The Fall of Unicorns and Sequential Bankruptcies: The Chilling Reality of U.S. Battery Startups in 2026

In a sharp reversal from the investment boom of the early 2020s, the U.S. battery industry in 2026 is facing a severe crisis marked by a wave of bankruptcies and the withdrawal of major investors from once-promising startups.

1. The Collapse of an Industry Icon: The Case of 24M Technologies

The closure of 24M Technologies, a company once valued at over 1 billion dollars (a “unicorn”), has sent shockwaves throughout the sector.

- Innovation: The company held technology to simplify conventional lithium-ion manufacturing and increase energy density through thick electrode layers. It famously aimed to achieve a driving range of 1,000 miles (approximately 1,600 kilometers).

- Background of Failure: Despite its technology being viewed as highly feasible due to its compatibility with existing chemistries, the company could not overcome the hurdles of mass production and sustained funding, leading to an asset auction.

2. A Series of Startup Exits

Beyond 24M, other high-profile companies that were once highly anticipated have been forced into shutdown or bankruptcy.

- Natron Energy: Once the U.S. flagship for sodium-ion batteries, it ceased operations in September 2025.

- Ample: A pioneer in EV battery swapping systems, it filed for bankruptcy in December 2025.

- Changing Investment Climate: Venture capital appetite for “innovation” has waned, leading to a stagnation in funding for novel, high-risk ideas.

3. Complex Factors Behind the Stagnation

The foundational pillars that supported the U.S. battery ecosystem are beginning to crumble.

- Policy Retreat: The gutting of key subsidies and incentives within the Inflation Reduction Act (IRA) has drastically reduced the attractiveness for investors.

- Cooling EV Market: Driven by a slowdown in consumer demand, automakers are canceling EV development programs and scaling back factory construction.

- Chinese Dominance: While the U.S. struggles, Chinese battery and EV manufacturers are further strengthening their global dominance through superior supply chains and cost competitiveness.

4. Remaining “Bright Spots”

Even in this harsh climate, growth potential remains in specific segments.

- Stationary Energy Storage Systems (ESS): While the EV sector struggles, the market for grid-scale storage systems remains on a growth trajectory, including within the U.S.

- Manufacturing Process Improvements: The importance of “manufacturing technologies directly linked to cost reduction”—the very goal 24M pursued—continues to be highly valued by surviving firms.

Comparison Summary: The Divergence of “Success” and “Failure”

| Item | Boom Period (2021-2023) | Current Stagnation (2026) |

| Funding | Massive capital flowed even to unverified technologies | Investors have turned conservative; capital withdrawal is accelerating |

| Primary Targets | Long-range EVs, novel chemistries (e.g., All-Solid-State) | ESS (Stationary Storage), cost reduction for existing tech |

| Policy Environment | Strong support through the IRA | Uncertainty in support due to the gutting of key legislation |

| Market Leaders | Proliferation of U.S. startups | Establishment of dominant positions by major Chinese firms |

コメント