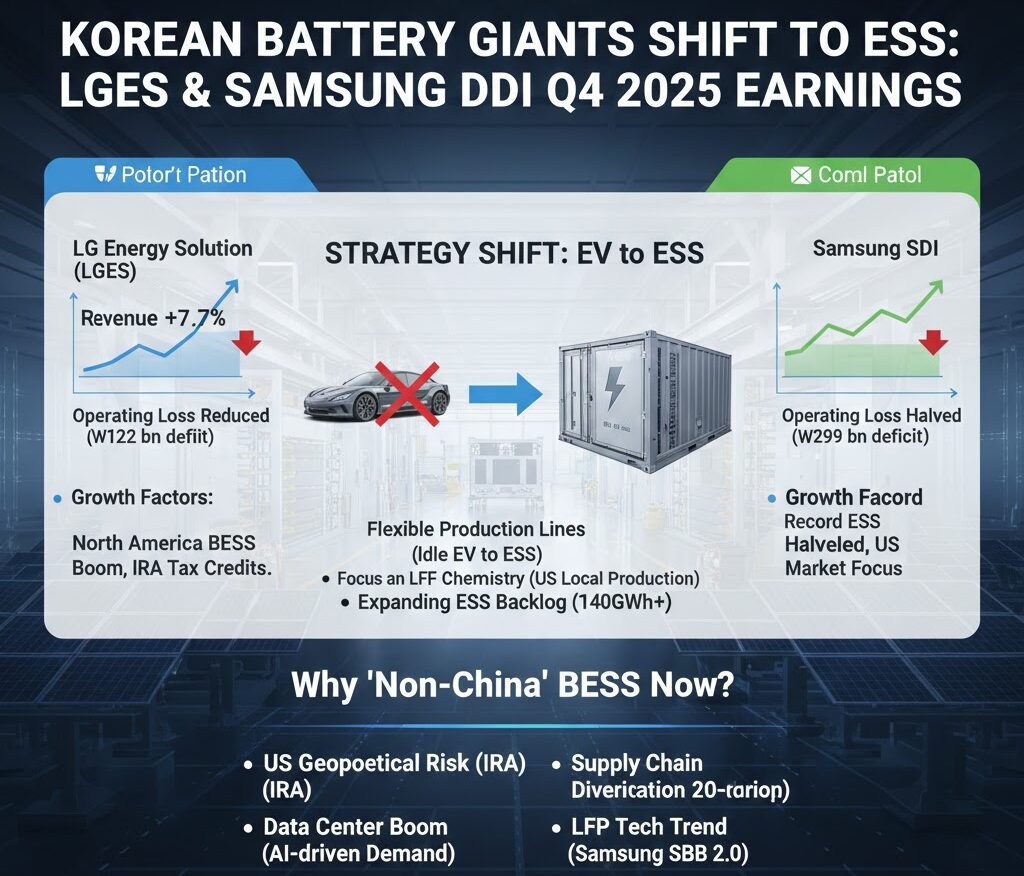

2025年第4四半期、韓国のバッテリー大手2社(LGES、サムスンSDI)は、電気自動車(EV)向け需要の停滞に直面しながらも、電力貯蔵システム(BESS / ESS)の劇的な売上増加により、営業損失を大幅に縮小させました。

1. 各社の業績ハイライト(2025年第4四半期)

| 項目 | LGエナジーソリューション (LGES) | サムスンSDI |

| 売上高 | 6兆1,000億ウォン (前四半期比 7.7%増) | 3兆8,600億ウォン |

| 営業損益 | 1,220億ウォンの赤字 (赤字幅が縮小) | 2,992億ウォンの赤字 (前四半期から半減) |

| 成長要因 | 北米でのBESS販売好調、IRA税額控除 | ESS製品の過去最高売上、米国市場への集中 |

2. 戦略の転換:EVからESS(エネルギー貯蔵)へ

両社はEV市場の一時的な停滞を乗り切るため、リソースをESSへ大胆に再配分しています。

- 生産ラインの柔軟な運用: LGESは、稼働率の低いEV用ラインをESS用に転換。ステランティスやホンダとの合弁工場の設備も一部活用し、資産の最適化を図っています。

- LFP(リン酸鉄リチウム)への注力: 安価で安全性が高いLFPバッテリーは、ESS市場の主流です。両社とも北米での現地生産体制を構築し、中国勢に対抗しています。

- 受注残の拡大: LGESは140GWhという膨大なESS受注残を抱えており、2026年にはさらに90GWhの新規受注を目指しています。

関連情報:なぜ今「非中国製」BESSが求められているのか?

ニュースの背景にある、現在の市場動向を補足します。

米国市場における地政学的リスク

米国では、エネルギーインフラにおける中国依存を減らすため、インフラ抑制法(IRA)などを通じて現地生産品に手厚い補助金を出しています。

- 供給網の多様化: 開発業者は、将来的な関税引き上げや規制リスクを避けるため、サムスンやLGのような「非中国系」サプライヤーとの長期契約を急いでいます。

- データセンターの急増: AI(人工知能)の普及に伴い、データセンター向けのバックアップ電源や、再生可能エネルギーの平準化に必要な大型蓄電池の需要が爆発的に増えています。

技術トレンドの移行

これまでは高価な三元系(NCA/NCM)が中心でしたが、現在はLFP(リン酸鉄リチウム)がESSの標準となりつつあります。韓国勢はこれまで三元系を得意としてきましたが、現在はサムスンの「SBB 2.0」のように、ESS向けLFP製品の量産を急ピッチで進めています。

注記: LGESの発表によると、米国での生産インセンティブ(税額控除)がなければ、損失額は4,550億ウォンまで膨らんでいた計算になります。これは、米国の政策が韓国メーカーの生命線となっている現状を浮き彫りにしています。

ESS Rescues Battery Giants from EV Slump: Samsung and LG Trim Losses Amid BESS Surge

In the fourth quarter of 2025, South Korea’s two leading battery manufacturers, LG Energy Solution (LGES) and Samsung SDI, significantly narrowed their operating losses. Despite facing a stagnation in demand for electric vehicle (EV) batteries, the companies saw a dramatic increase in sales from Battery Energy Storage Systems (BESS/ESS).

1. Financial Highlights (Q4 2025)

| Item | LG Energy Solution (LGES) | Samsung SDI |

| Revenue | 6.1 trillion KRW (Up 7.7% QoQ) | 3.86 trillion KRW |

| Operating Profit/Loss | Loss of 122 billion KRW (Narrowed) | Loss of 299.2 billion KRW (Halved QoQ) |

| Growth Drivers | Strong North American BESS sales, IRA tax credits | Record-high ESS sales, focus on US market |

2. Strategic Pivot: From EV to ESS (Energy Storage)

To navigate the temporary “chasm” in the EV market, both companies are aggressively reallocating resources toward the ESS sector.

- Flexible Production Lines: LGES is converting underutilized EV production lines for ESS use. They are also optimizing assets by temporarily utilizing production lines from joint ventures with Stellantis and Honda.

- Focus on LFP (Lithium Iron Phosphate): LFP batteries, known for lower costs and high safety, have become the ESS market standard. Both companies are establishing local production in North America to compete with Chinese manufacturers.

- Growing Order Backlog: LGES currently holds a massive ESS order backlog of 140 GWh and aims to secure an additional 90 GWh in new orders during 2026.

Background: Why the Demand for “Non-Chinese” BESS is Surging

The following market trends provide context to the recent news:

Geopolitical Risks in the US Market

To reduce reliance on China for energy infrastructure, the US government provides significant subsidies for locally manufactured products through the Inflation Reduction Act (IRA).

- Supply Chain Diversification: Project developers are rushing into long-term contracts with “non-Chinese” suppliers like Samsung and LG to mitigate risks associated with future tariff hikes and regulatory changes.

- Data Center Explosion: With the rapid expansion of AI (Artificial Intelligence), there is an explosive demand for backup power sources for data centers and large-scale batteries to stabilize renewable energy grids.

Shift in Technology Trends

While expensive ternary batteries (NCA/NCM) were previously the standard, LFP (Lithium Iron Phosphate) is now becoming the norm for ESS. Although Korean manufacturers have traditionally specialized in ternary chemistry, they are now fast-tracking the mass production of LFP products for the ESS market, such as Samsung SDI’s “SBB 2.0.”

Note: According to LGES, their losses would have expanded to 455 billion KRW without the US production incentives (tax credits). This highlights how vital US policy has become to the survival of South Korean battery makers.

コメント