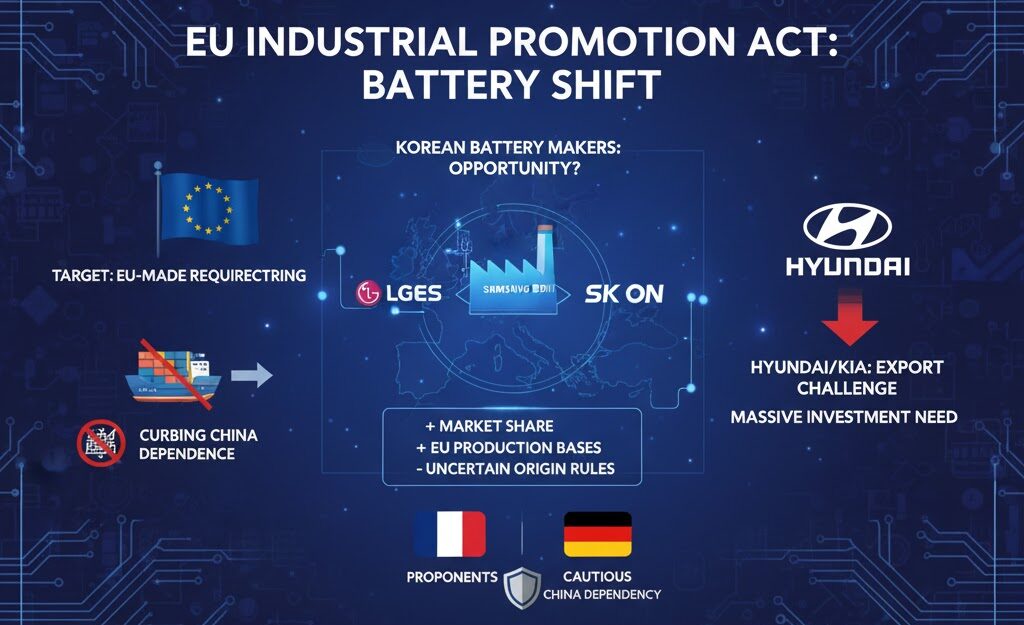

欧州連合(EU)が発表した産業促進法(IAA)の最終案は、域内のクリーンエネルギー産業(EV・バッテリー等)を保護し、中国への依存度を低減させることを目的としています。これを受け、韓国のバッテリー大手3社(LGエナジーソリューション、サムスンSDI、SKオン)は、失った市場シェアを奪還する好機と捉え、動向を注視しています。

1. 主な政策内容と「ドラギ報告書」の背景

この政策は、米国が実施しているインフレ抑制法(IRA)の欧州版とも言える内容です。

- 現地生産要件: 製品が「EU製」と認められ、補助金等の支援を受けるには、部品の少なくとも70%をEU域内で組み立てる必要があります。

- 目標数値: EUのGDPに占める製造業の割合を、現在の14%から20%へ引き上げることを目指しています。

- 対中規制: 特定分野で世界シェア40%を超える国(現状は中国のみ)の企業に対し、欧州への投資時に厳格な承認手続きを義務付けます。これは、中国企業が工場を欧州に移すだけで規制を逃れる「抜け道」を塞ぐ狙いがあります。

2. 韓国バッテリー業界への影響:期待と課題

韓国企業にとって、今回の政策は「諸刃の剣」となる可能性があります。

- シェア回復のチャンス: 2022年に欧州市場で80%のシェアを誇っていた韓国勢ですが、安価な中国製(LFPバッテリー等)の流入により、現在は30%台まで低下しています。中国製品が排除されれば、再び優位に立てる可能性があります。

- 既存拠点の活用: 韓国3社はすでにハンガリーやポーランドに大規模な生産拠点を構えており、現地生産要件(70%ルール)への対応において他国企業より一歩リードしています。

- 不透明な「原産地規則」: 韓国はEUと自由貿易協定(FTA)を締結していますが、今回の案では「韓国産」が自動的に「EU産」とみなされるわけではありません。最終的な定義次第では、さらなる追加投資を迫られるリスクがあります。

3. 自動車業界(現代自動車グループ)の苦境

バッテリー業界とは異なり、完成車メーカーの現代自動車(Hyundai)や起亜(Kia)には懸念が広がっています。

- 輸出モデルの制限: 現在、アイオニック5(IONIQ 5)やEV6などの主力EVの多くは韓国国内で生産し、欧州へ輸出しています。新政策が適用されると、これらが補助金対象から外れる恐れがあります。

- 投資負担の増大: 欧州内(チェコ、スロバキア)の既存工場の生産能力には限りがあり、要件を満たすためには莫大な追加投資を行って生産ラインを移管する必要があります。

4. EU内部の足並みの乱れ

この政策の行方は、EU加盟国間の利害対立にも左右されます。

| 立場 | 主な国 | 理由 |

| 推進派 | フランス、イタリア | 自国の製造業保護と、中国製EVの流入阻止を優先。 |

| 慎重・反対派 | ドイツ | メルセデス・ベンツやBMWなどが中国市場に深く依存しており、中国側からの報復(関税引き上げ等)を恐れている。 |

関連情報:市場のコンテキスト

- EV市場の減速(キャズム現象): 現在、世界的にEV需要が一時的に停滞しており、SKオンが無給休暇を導入するなど、韓国メーカーも経営の舵取りに苦慮しています。この法案が需要回復の起爆剤になるかが注目されています。

- 相互主義の懸念: 韓国政府側は、「韓国は生産地に関わらずEV補助金を出しているのに、EUが現地生産を義務付けるのは不公平(相互主義に反する)」として、今後交渉を行う構えです。

“European IRA” Provides Tailwinds for South Korea; Aiming to Reclaim Market Share by Excluding Chinese Batteries

The final draft of the Industrial Advancement Act (IAA) announced by the European Union (EU) aims to protect the regional green energy industry (EVs, batteries, etc.) and reduce dependence on China. In response, South Korea’s three major battery manufacturers (LG Energy Solution, Samsung SDI, and SK On) view this as a prime opportunity to reclaim lost market share and are closely monitoring the situation.

1. Key Policy Details and Background of the “Draghi Report”

This policy is essentially the European version of the Inflation Reduction Act (IRA) implemented by the United States.

- Local Production Requirements: To be certified as “Made in the EU” and qualify for subsidies or support, at least 70 percent of EV components must be assembled within the EU.

- Target Figures: The policy aims to increase the share of manufacturing in the EU’s GDP from the current 14 percent to 20 percent.

- Regulations Against China: Companies from countries with a global market share exceeding 40 percent in specific sectors (currently only China) must undergo strict approval procedures before investing in Europe. This is intended to close “loopholes” where Chinese companies bypass regulations simply by building factories in Europe.

2. Impact on the South Korean Battery Industry: Opportunities and Challenges

For South Korean companies, this policy could be a double-edged sword.

- Chance to Reclaim Market Share: South Korean firms held an 80 percent share of the European market in 2022, but this has dropped to the 30 percent range due to the influx of cheap Chinese batteries (such as LFP batteries). If Chinese products are excluded, South Korean firms may regain their dominance.

- Leveraging Existing Bases: The three major South Korean manufacturers already have large-scale production bases in Hungary and Poland, giving them a head start in meeting the 70 percent local production requirement.

- Uncertainty Over “Rules of Origin”: Although South Korea has a Free Trade Agreement (FTA) with the EU, the current proposal does not automatically classify “Made in Korea” products as “Made in the EU.” Depending on the final definitions, there is a risk of being forced to make significant additional investments.

3. Struggles for the Automotive Industry (Hyundai Motor Group)

Unlike the battery industry, concerns are mounting for finished vehicle manufacturers like Hyundai and Kia.

- Restrictions on Export Models: Currently, many flagship EV models such as the IONIQ 5 and EV6 are manufactured in South Korea and exported to Europe. Under the new policy, these models may no longer qualify for subsidies.

- Increased Investment Burden: Production capacity at existing plants in Europe (Czech Republic, Slovakia) is limited. To meet the requirements, companies may need to invest massive amounts of capital to relocate production lines.

4. Internal EU Disagreements

The future of this policy depends on the conflicting interests of EU member states.

| Position | Key Countries | Reason |

| Proponents | France, Italy | Prioritize protecting domestic manufacturing and blocking the influx of Chinese EVs. |

| Cautions / Opponents | Germany | Heavily dependent on the Chinese market (e.g., Mercedes-Benz, BMW) and fear retaliation such as tariff hikes from China. |

Related Information: Market Context

- EV Market Slowdown (Chasm Phenomenon): Global EV demand is currently stagnant. South Korean manufacturers are struggling, with SK On introducing unpaid leave for employees. All eyes are on whether this bill will act as a catalyst for a demand recovery.

- Concerns Over Reciprocity: The South Korean government argues that while South Korea provides EV subsidies regardless of the production location, the EU’s local production mandate is unfair and violates the principle of reciprocity. They plan to raise this issue in future negotiations.

コメント