ワシントン(米政府)の政策において、バッテリー産業は極めて重要であるにもかかわらず、法案や大統領令の中で「括弧書き(副次的な扱い)」に追いやられていると、業界リーダーたちが警告しています。これまでの「補助金による支援」の時代は終わり、政府が株式取得や取引を通じて直接介入する「ディールメイキング(投資家)」の時代へと変化しています。

1. 政策上の「括弧書き」問題

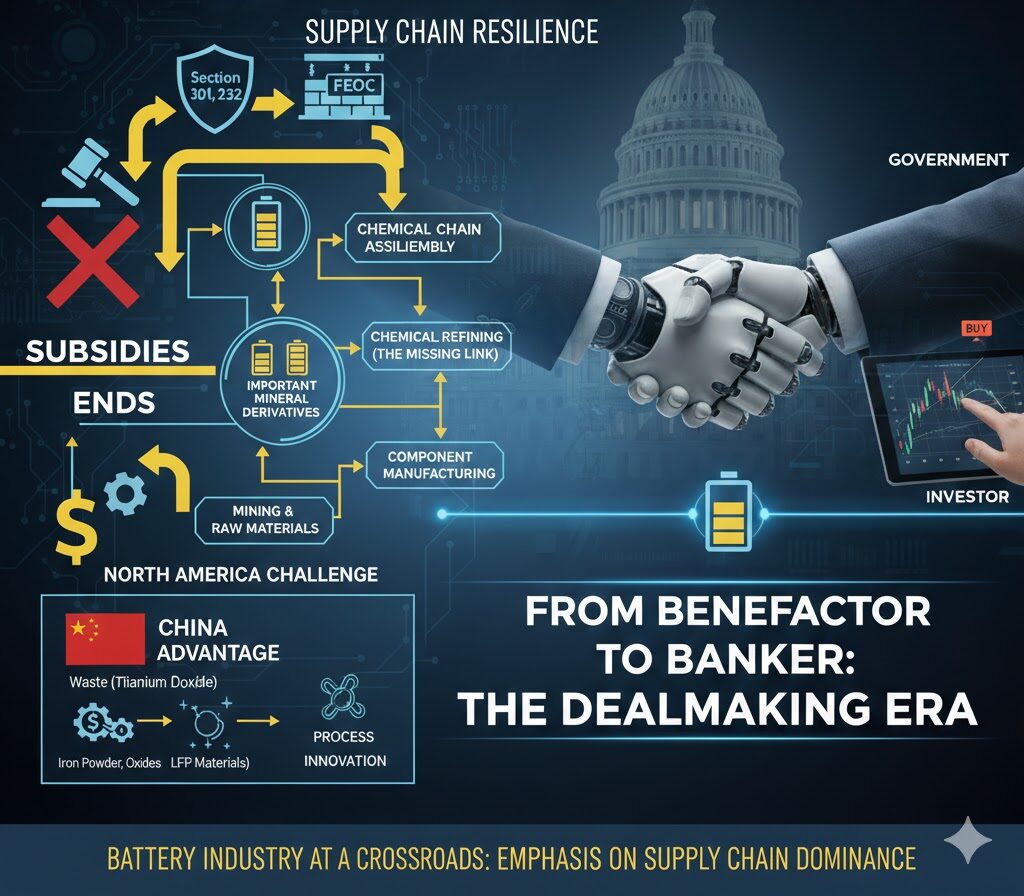

- 現状: 政策文書において、バッテリーは「重要鉱物の派生製品」という注釈的な扱いに留まっています。

- 変化: 大規模な補助金(無償資金協力)から、関税(第301条、第232条)や「懸念される外国の事業体(FEOC)」規制を駆使した、貿易第一主義の行政措置へ移行しています。

2. 政府の役割の変化:恩人から銀行家へ

- 投資形態: 政府は単なる助成金の提供者ではなく、プロジェクトの株式を取得したり、価格下限を支持したりする「政府系ファンド」のような役割を強めています。

- 事例: MP Materialsのような企業との取引に見られるように、民間企業は政府を「株主」として交渉する能力が求められています。

3. サプライチェーンの「ミッシング・リンク」

- 中国の優位性: 中国は、二酸化チタン生産時の廃棄物(硫酸鉄)をLFP(リン酸鉄リチウム)バッテリーの原料に転換する独自の産業エコシステムを構築しています。

- 北米の課題: 北米には同様の廃棄物備蓄がないため、中国の技術をコピーするだけでは不十分です。鉄粉や酸化物など、自国にある原料を活用する「プロセスイノベーション」が不可欠です。

4. 防衛部門による技術実証の促進

- レジリエンス・プレミアム: 自動車市場は価格に敏感ですが、防衛部門(DoD)や産業部門は「セキュリティ(供給の安定)」にコストを払う準備があります。

- 触媒としての役割: 軍事利用を通じて新しい化学組成やサプライチェーンの有効性を証明することが、民間市場への普及を助ける触媒となります。

関連情報:業界を取り巻く追加背景

1. 中国の「5カ年計画」に対抗する難しさ

中国のバッテリー支配は、数十年にわたる一貫した国家政策(14次にわたる5カ年計画)の成果です。一方、米国は選挙サイクルごとに政策が変動しやすく、長期的な産業戦略の維持が最大の課題となっています。

2. 「機械を作るための機械」の関税リスク

バッテリー製造に必要な高度な設備(資本設備)の多くを海外に依存している場合、対中関税がブーメランとなり、自国内のギガファクトリー建設コストを押し上げるリスクがあります。

3. 中間精製工程の不足

現在、世界中に「鉱山」と「完成車工場」は増えていますが、原鉱石をバッテリーグレードの材料に精製する「化学精製能力」がアジア(特に中国)に集中しています。この「中流工程」の確保が、北米の真の自立の鍵となります。

Resilience Over Capacity: Bridging the Midstream Gap in the North American Battery Chain

Industry leaders are warning that despite its critical importance, the battery industry is being pushed into “parentheses” (secondary status) within Washington’s legislative bills and executive orders. The era of simple “support through subsidies” has ended, giving way to an era of “deal-making,” where the government intervenes directly through equity stakes and strategic trade agreements.

1. The “Parentheses” Problem in Policy

- Current Status: In policy documents, batteries are often relegated to a footnote, referred to merely as “derivatives of critical minerals.”

- The Shift: The focus has moved from massive grants (free capital) to trade-first administrative actions, utilizing tariffs (Section 301 and 232) and “Foreign Entity of Concern” (FEOC) regulations.

2. Evolution of the Government’s Role: From Benefactor to Banker

- Investment Style: The government is acting more like a “sovereign wealth fund” rather than a simple grant provider, increasingly taking equity in projects or providing price-floor support.

- Case in Point: As seen in deals with companies like MP Materials, private firms must now develop the capability to negotiate with the government as a “shareholder.”

3. The Supply Chain’s “Missing Link”

- China’s Dominance: China has built a unique industrial ecosystem that converts iron sulfate waste from titanium dioxide production into raw materials for LFP (Lithium Iron Phosphate) batteries.

- North American Challenges: Since North America lacks similar waste stockpiles, simply copying Chinese technology is insufficient. “Process innovation” is essential to utilize locally available raw materials, such as iron powder or oxides.

4. Defense Sector as a Catalyst for Technology Validation

- The Resilience Premium: While the automotive market is highly price-sensitive, the defense (DoD) and industrial sectors are prepared to pay a premium for “security” (supply stability).

- Role as a Catalyst: Utilizing military applications to prove the viability of new chemistries and supply chains serves as a catalyst for adoption in the broader commercial market.

Related Information: Additional Industry Context

1. Challenges in Competing with China’s “Five-Year Plans”

China’s battery dominance is the result of decades of consistent national policy (spanning 14 Five-Year Plans). In contrast, U.S. policy often fluctuates with every election cycle, making the maintenance of a long-term industrial strategy the greatest challenge.

2. Tariff Risks for “Machines that Make the Machines”

Because many advanced tools (capital equipment) required for battery manufacturing are sourced from abroad, tariffs against China can act as a boomerang—risking a spike in the construction costs of domestic gigafactories.

3. Lack of Midstream Refining Capacity

While “mines” and “vehicle assembly plants” are increasing globally, the “chemical refining capacity” to turn raw ore into battery-grade materials remains concentrated in Asia (specifically China). Securing this “midstream” process is the key to true independence for North America.

コメント